Listen to this Insight

Despite strong local returns, a global energy shock, rapidly rising rates, and elevated geopolitical risks, Japanese equities offer significant upside driven by deep-seated structural reforms, improving fundamentals, and attractive valuation opportunities.

Executive Summary

For the last eight years, GMO’s Asset Allocation team has held a differentiated view on Japanese equities. Long before Japan re‑entered the global investment narrative, we argued that the country was undergoing slow but durable structural changes aimed at improving corporate governance, growth, and capital efficiency. These reforms were never expected to deliver quick results. Instead, we expected them to compound quietly over time.

Today, the evidence is clear: Japanese companies have meaningfully improved profit margins, delivered strong earnings growth, and shifted attitudes toward shareholders’ interests. Many investors, though, remain concerned that the Japanese equity market is no longer cheap given strong recent returns, that it is overly exposed to higher oil prices and geopolitical risks, and that corporate reform pressures may abate.

Investors also worry about the impact of higher interest rates given Japan’s high gross debt. While rising rates increase the risk of volatility and potential squeezes on government finances, Japan’s low net debt—bolstered by substantial assets and domestic ownership—combined with the Bank of Japan's likely moderate approach to potential rate rises, should allow the policymakers to manage the situation effectively.

We see numerous reasons to continue to overweight Japan equities:

- Corporate reform momentum is accelerating, lifting return on equity (ROE) and shareholder returns with more runway ahead.

- The cheap yen provides two ways to win.

- Active investors narrowing their underweight positions could provide a tailwind.

- Valuations offer refuge in an otherwise expensive world.

We believe investors should be selective and active in their Japan equity exposure. We suggest focusing on the segment of the market that is truly dislocated—small value—and being active to benefit from the dramatic inefficiencies in Japan and the opportunity to drive shareholder outcomes through engagement.

Japan’s Improvements Are Durable and Impactful

Japan’s reform process began in earnest with the late 2012 re-election of Prime Minister Abe. Policymakers and regulators had set out to address chronic weaknesses in Japan’s economic and corporate ecosystems: an embedded deflationary mindset, persistently low profitability, inefficient balance sheets, and limited accountability to shareholders. These shortcomings were the legacy of decades of balance sheet repair following the massive bubble in the 1980s, which led management teams to prioritize stability, employment, and stakeholder harmony over capital efficiency.

Over time, a broad and reinforcing framework of reforms emerged. Governance and stewardship codes raised expectations around board independence and investor dialogue. Asset owners and proxy advisors became more vocal. The Tokyo Stock Exchange increased pressure on companies trading below book value and with subpar ROE to articulate concrete plans for improvement. More recently, initiatives aimed at capital markets, labor flexibility, and corporate restructuring have emphasized the same message: capital must earn an appropriate return.

Importantly, these changes have not been superficial. Japanese companies have undertaken difficult operational improvements—raising prices in historically price‑sensitive markets, cutting costs, divesting non‑core assets, and streamlining business portfolios. The cumulative effect has been a sustained improvement in margins, profitability, and ROE across large segments of the market. As a result, Japanese companies have delivered robust earnings-per-share growth over the last decade while meaningfully outpacing nominal GDP growth. Earnings growth in Japan has been impressively stronger than in the “exceptional” U.S. 1

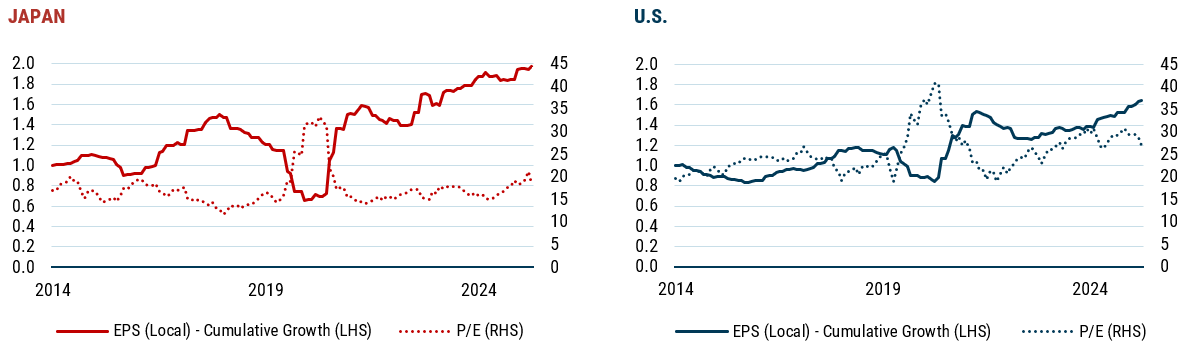

Exhibit 1: EPS Growth vs. P/E Ratios by Region

As of 12/31/2025 | Source: GMO, Worldscope, Compustat, MSCI Indexes

MSCI data may not be reproduced or used for any other purpose. MSCI provides no warranties, has not prepared or approved this report, and has no liability hereunder. Please visit https://www.gmo.com/americas/benchmark-disclaimers/ to review the complete benchmark disclaimer notice.

Japan Snaps Back

Strong earnings growth has translated into strong returns. Since we shared a constructive outlook for Japan at our 2018 GMO Conference, the MSCI Japan index has compounded at a 14.2% annualized rate. 2 We estimate that nearly two-thirds of this return came from the aforementioned fundamental improvements, leaving about one-third from valuation changes. Markets have rewarded fundamental improvements by increasing Japan’s price to earnings (P/E) from 13x at the beginning of the period to 18.5x at the end.

After a period of strong fundamentals and valuation expansion, investors are rightly asking how much gas is left in the Japanese equity tank. In short, meaningful opportunity remains. While Japan’s P/E is no longer screamingly cheap, it’s far from expensive. And with a 20% discount to the U.S. (based on price to forward earnings), Japan still looks like a relative bargain. Japan looks 40-60% cheaper, in fact, on non-earnings-based metrics such as price to sales, price to gross profit, and price to book value—discounts that could narrow if Japanese companies continue to raise margins toward developed-market norms. Further, dispersion within the Japanese market remains wide, creating fertile ground for active investors. We see a number of reasons to expect Japanese stocks, and Japan’s small value stocks in particular, to continue benefiting investor portfolios in the years ahead.

Why Japanese Equities Still Look Compelling

- Corporate reform momentum is accelerating, lifting ROE and shareholder returns with more runway ahead.

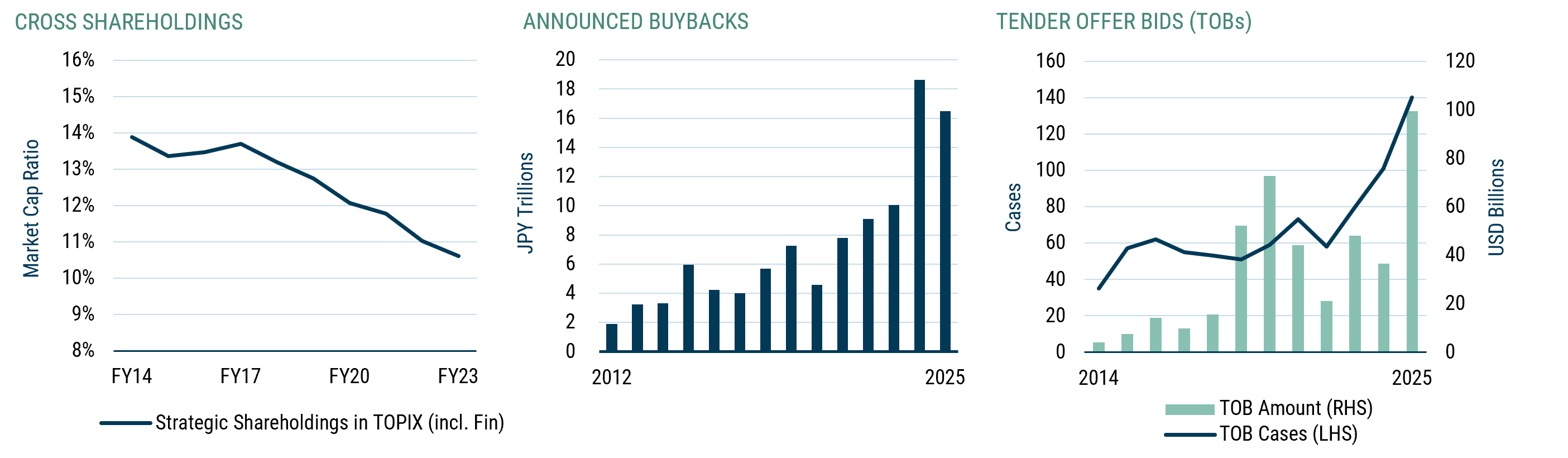

Recent ROE improvements have come primarily from margin expansion and operational discipline. While Japan’s profit margins have trended in the right direction, we believe substantial upside remains, boosted by an accelerated phase of corporate governance reforms. Reform is increasingly embedded in both boardrooms and regulation: management teams have shifted toward ROE improvement, disciplined capital allocation, and deeper shareholder engagement (e.g., boards now commonly comprise at least one-third independent directors, strategic cross holdings have declined, and dividends and buybacks have risen).

Other encouraging signs of reform include the adoption of more aggressive change-of-control tactics. GMO’s Usonian Japan Equity team, who has been on the ground investing in and engaging with management teams for over 20 years, has never seen the market for corporate control so active. In 2025 alone, 5 of the 40 or so companies in GMO’s Usonian Japan Value Strategy were subject to tender offers at significant premiums, and the pace of such conversations across the portfolio remains robust today. We have also noted encouraging new trends of structural realignment between companies and shareholders, including industry consolidation and the spin-out of non-core assets.

EXHIBIT 2: GENERATIONAL STRUCTURAL REFORMS

Source: JPMorgan, Quick, Recof

Momentum behind these tailwinds is accelerating as policymakers sharpen expectations. April draft revisions from the Financial Services Agency and the Tokyo Stock Exchange push governance from box ticking to substance by pressuring boards, especially at cash-rich firms, to clearly justify retained capital within a coherent growth strategy (investment, restructuring, or returns). For investors, the key is not a one-off boost to payouts, but a sustained increase in capital productivity and a stronger translation of Japan’s macro normalization into higher underlying returns on capital, albeit within a framework that still balances shareholder outcomes with public interest considerations.

- The cheap yen provides two ways to win.

The yen trades near multi-decade lows on purchasing power parity measures. For non-yen investors, this currency undervaluation represents a potential additional source of return. Overseas investors will benefit from the appreciation of unhedged Japanese equity holdings if the yen reverts to fair value, while a sustained weak yen would continue to support exporters’ earnings growth. Importantly, this currency tailwind operates largely independently of current equity valuations. GMO’s 7-Year Asset Class Forecast implies a healthy 10.5% real return for the Japan small value group when measured in U.S. dollars. 3 - Active investors narrowing their underweight positions could provide a tailwind.

Despite improving fundamentals, global investor positioning in Japan remains cautious, reflecting skepticism shaped by decades of disappointment. While sentiment has improved, ownership levels still suggest room for incremental reallocation. Of 203 actively managed strategies in the eVestment database that list the MSCI EAFE index as their preferred benchmark, 74% are underweight Japan by an average of 6.5%. 4 The gap between fundamentals and positioning matters: even incremental re‑allocation toward Japan could provide a durable tailwind to valuations over time. - Valuations offer refuge in an otherwise expensive world.

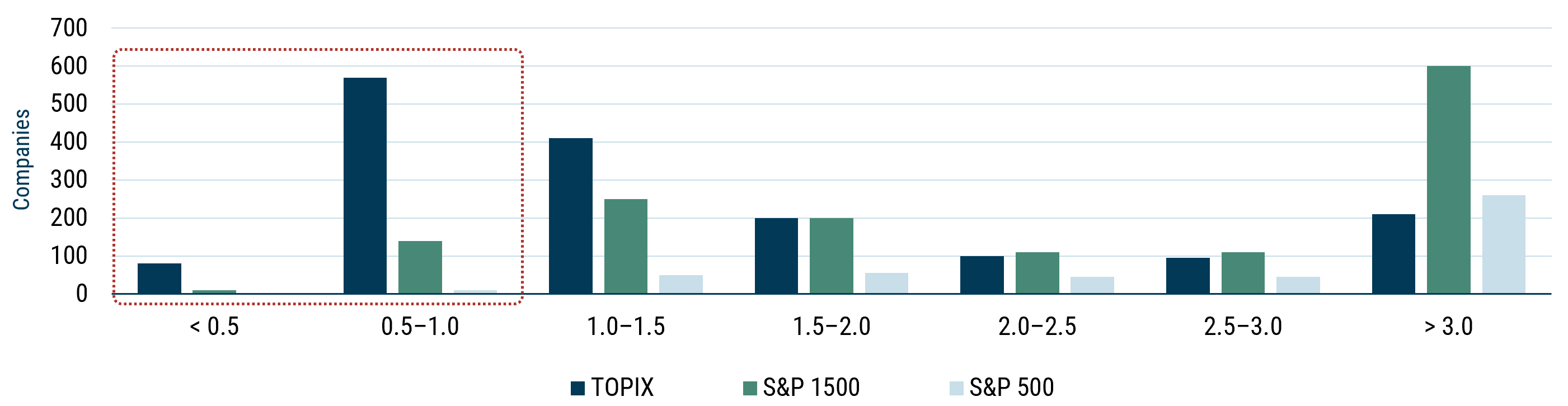

After a period of strong local returns with some multiple expansion, the broad equity market in Japan now trades at 16.1x price to forward earnings, 5 which is a modest premium to its trailing 25-year average. While that may suggest broad Japanese equities are fully valued on an absolute basis, Japan has two things going for it from a valuation perspective. First, Japanese equities trade significantly cheaper than U.S. equities, as noted. Second, within Japan, valuation dispersions remain unusually wide. Small value stocks are particularly attractive, trading at a deep 38% discount to the market and at a 23rd-percentile valuation relative to history, making them cheap in absolute and relative terms.

With nearly 4,000 publicly traded companies, Japan offers an unusually broad opportunity set of undervalued businesses, particularly outside the largest index constituents. Even after a strong market rally, nearly 40% of listed companies on the TOPIX trade below book value—a striking statistic for a developed market. Many of these businesses are profitable, asset‑rich, and conservatively financed.

EXHIBIT 3: COMPANIES BY PRICE TO BOOK VALUATION

As of 12/31/2025 | Source: FactSet

Capitalizing on the Opportunity: Be Selective and Active

We believe investors should be selective and active in their Japan equity exposure. Instead of gaining exposure to Japan through broad index funds, where valuations appear fair to modestly expensive, investors should focus on small value stocks to capitalize on the group’s abnormally wide discount. We also advocate leaning enough into the opportunity to have an impact at the portfolio level (our positioning across strategies certainly reflects this view). In our most flexible GMO Benchmark-Free Allocation Strategy, our equity book has approximately 4.5x the MSCI ACWI’s weight in Japan, reflecting our conviction that the opportunity is structural rather than cyclical.

Further, Japan is a market where active management can benefit investors. Japan remains the third‑largest equity market globally, with thousands of companies spanning a wide range of industries and market capitalizations. Yet despite its size, it remains one of the least efficiently researched major markets. Analyst coverage drops sharply outside the largest index constituents, leaving hundreds of small and midcap companies lightly followed or ignored altogether by global investors.

GMO’s Asset Allocation team taps into opportunities in Japan through both quantitative investment approaches, which we believe are well-suited to the market, and fundamental approaches, which together provide diversifying sources of alpha.

Japan is a fertile investment environment for the specialized, engagement‑oriented skill set that sits at the core of our Usonian Japan Equity team’s investment philosophy. The team manages the largest component of the GMO Benchmark-Free Allocation Strategy’s Japan exposure. Composed of both Japanese and American investors, GMO’s local language fluency, cultural context, and long‑standing relationships enable access and credibility, while our external perspective helps challenge entrenched assumptions.

The investment process is value‑led and catalyst‑driven. Engagement is constructive rather than confrontational, emphasizing persistent dialogue, achievable improvements, and alignment with Japan’s evolving policy framework. In a market rich with under‑optimized companies, this approach can materially accelerate value realization.

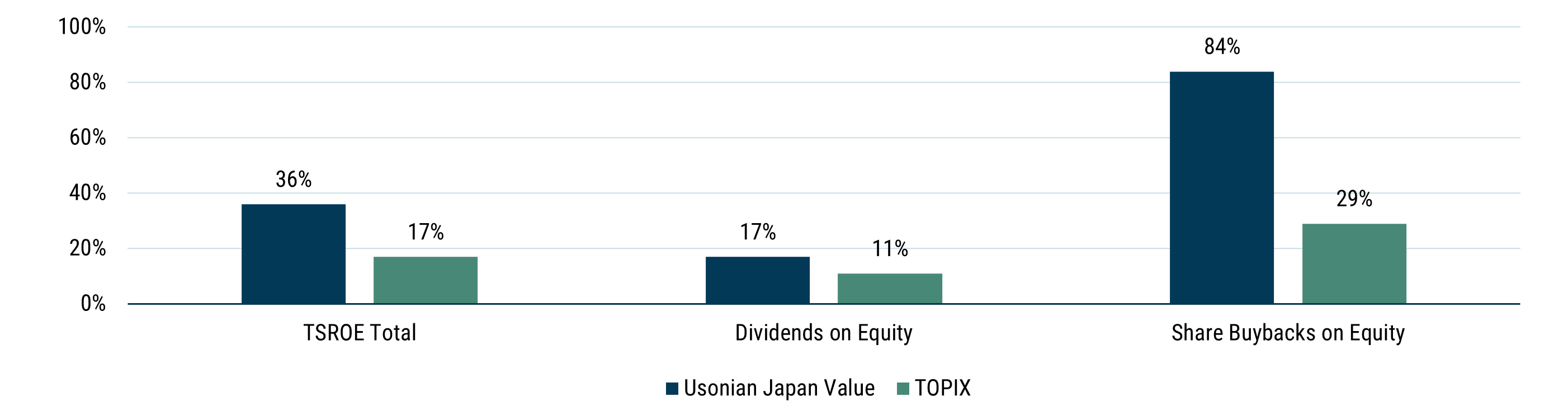

GMO’s Usonian Japan Equity team has a proven ability to drive positive change for shareholders. As Exhibit 4 suggests, the team has increased the total shareholder ROE for portfolio companies well above the improvement seen in the broader market.

EXHIBIT 4: ENGAGING FOR INFLUENCE

Growth in Average Total Shareholder Return on Equity (TSROE) and Composition Over Holding Period

Analysis covers period from December 2011 through March 2026

Conclusion: The Opportunity Remains Intact

Japan’s equity story is no longer about latent potential alone. Tangible improvements in earnings, profitability, and governance are evident. At the same time, valuations, investor positioning, and capital allocation behavior suggest the opportunity remains both underappreciated and nuanced.

From our perspective, Japan is not in the late innings of a trade. It is still in the middle innings of a long game, one that increasingly rewards selectivity, engagement, and active ownership rather than broad market exposure. While we may continue to see episodic volatility driven by geopolitical developments and energy markets, the influence of reforms has gained momentum at the company level and does not depend on a benign macro or geopolitical environment. For investors willing to look past outdated narratives, we believe Japan remains a compelling source of long‑term value creation.

It’s worth noting that much of this change occurred without the “help” of U.S. private equity firms—a topic eloquently chronicled by our friend Andrew McDermott (available on Jesper Koll’s Japan Optimist Substack).

10/31/2018–4/30/2026.

As of 3/31/2026, under the GMO Asset Allocation team’s “low” forecast scenario, which assumes a terminal cash rate equal to the rate of inflation.

As of 3/31/2026.

As of 3/31/2026.

Disclaimer: The views expressed are the views of Rick Friedman and John Thorndike through the period ending May 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2026 by GMO LLC. All rights reserved.

It’s worth noting that much of this change occurred without the “help” of U.S. private equity firms—a topic eloquently chronicled by our friend Andrew McDermott (available on Jesper Koll’s Japan Optimist Substack).

10/31/2018–4/30/2026.

As of 3/31/2026, under the GMO Asset Allocation team’s “low” forecast scenario, which assumes a terminal cash rate equal to the rate of inflation.

As of 3/31/2026.

As of 3/31/2026.