Overview

Equity and fixed income markets continue to look expensive, and expected returns are generally low. In contrast, resource equities are historically cheap and offer much higher potential returns. In addition to attractive returns, resource equities offer investors diversification, inflation protection, a margin of safety, inefficiencies, and optionality.

In this webcast, Lucas White, lead portfolio manager of the GMO Resources Strategy, discussed these opportunities.

Contact Us to Watch the Replay*

*This content is intended for accredited investors only.

Key Points

- The strategic case for resource equities is extremely compelling, offering investors the potential for excess returns, diversification, and inflation protection.

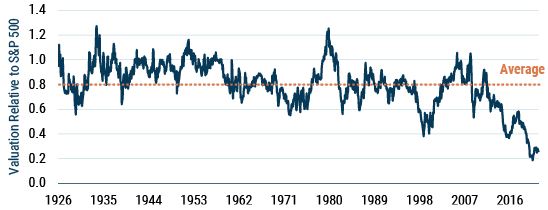

- Tactically, commodity producers are the cheapest they’ve been in the last 100 years on some measures, even as inflation has ticked up to 7% by the end of 2021.

- There’s a strong bull case for commodities today, but you don’t have to believe commodity prices are going to rise to make a solid case for owning resource equities. At current commodity prices, resource companies should generate extraordinary returns going forward.

- The energy transition is creating exciting opportunities for resource equities in the materials that drive clean energy solutions, such as copper, lithium, and nickel. Meanwhile, fossil fuels will be around for many years to come.

- We have a unique strategy that is well positioned to capitalize on these opportunities and has outperformed its benchmark by 750 bps, annualized, since its inception 10 years ago (net of fees). The portfolio’s holdings trade at historic discounts to the overall market, presenting investors with tremendous opportunities.

A One in a Hundred Year Opportunity?

Valuation of energy/metals companies relative to the S&P 500

As of 12/31/2021 | Source: S&P, MSCI, Moody’s, GMO

Valuation metric is a combination of P/E (Normalized Historical Earnings), Price-to-Book Value, and Dividend Yield.

Download event highlight here.