In recent years we have witnessed a surge in sovereign bond defaults in emerging markets. This is unfortunate because when a country defaults, almost everyone loses (aside from restructuring advisory and law firms). Creditors lose for sure. So does the country’s citizenry, which has likely felt the ill effects of the slippery slope into default and then also the aftereffects, such as higher borrowing costs and, therefore, investment return hurdles.

At GMO, however, we evaluate everything as a potential opportunity. In this case, the unusually high default rate and resulting low bond prices present a terrific total return opportunity among defaulted and distressed emerging debt issues.

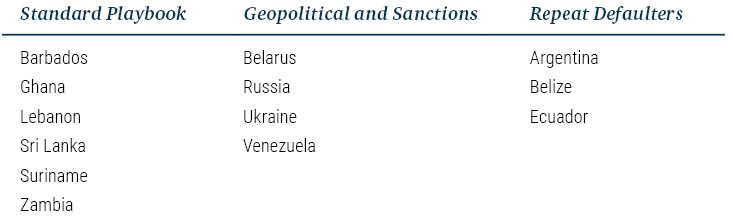

In the past five years, we count 13 instances of sovereign default in countries with an international bond market presence, a significant increase on the historical average default rate of about one per year. 1 When evaluating each sovereign default within our emerging debt investment process, we consider the path to default because different paths imply different likely outcomes. In Exhibit 1, we categorize recent defaults into three path-to-default groups: the “standard playbook” or traditional defaults, the “geopolitical and sanctions” group, and the “repeat defaulters.”

Exhibit 1: Three Categories of Recent Sovereign Defaults

The standard playbook default is the most, well…standard of the categories. These are countries that simply became addicted to fiscal deficits and debt financing. Interestingly, most of these countries had decent reputations in the markets and a strong willingness to pay. The story goes like this: over time, debt creeps higher and is increasingly used to finance current spending such as government wages and interest payments, rather than capital spending that might increase economic growth and, by extension, tax revenues to service the debt. Then, some shock comes along that fairly suddenly throws the country into the abyss of debt crisis. In all these cases, except for Barbados and possibly Lebanon, the shock this time was the combination of Covid-19 and Russia’s war in Ukraine.

This brings us to the geopolitical and sanctions defaulters. Unlike the first group, these countries often have relatively low debt. 2 Indeed, it is our view that none of these countries would be in default were it not for the financial sanctions imposed upon them by Western governments (albeit because of the countries’ own actions). Each of the four noted cases is a little different. Russia is the clear aggressor and violator of international law. Belarus is the accomplice. Ukraine is the invaded country, suffering devastating economic losses (its inclusion in this group is because its default is directly related to the aggression against it). Venezuela is a more curious example. It is deemed an illegitimate criminal regime by powerful political forces within the U.S. government. Sanctions inhibit investors from transacting in the secondary market for Venezuelan bonds and prevent bondholders from negotiating any sort of debt restructuring.

Finally, we have the repeat defaulters. It turns out that a leading indicator of whether a country will default in the future is whether it has defaulted in the past. When a country defaults, its reputation in the markets is tarnished – not forever, but for an extended period of time. When the Covid-19 shock hit the markets in March and April of 2020, Argentina, Belize, and Ecuador were among the first countries to capitulate and seek debt relief. This is likely because they knew market financing would be costly for them, given their past default history. In contrast, dozens and dozens of other countries with better payment records were able to fund part of the Covid-19 shock by issuing international bonds over the course of 2020 and 2021. It’s a cautionary tale for countries contemplating default, and a reason why many countries treat default as an absolute last resort (Sri Lanka and Ghana, among others, are good examples).

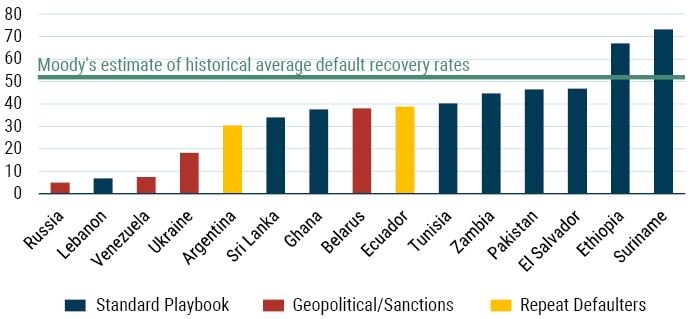

We are conditioned to be looking for signs about the first and third paths, but the second path (geopolitics and sanctions) is somewhat less predictable, not to mention more damaging to asset prices as shown in Exhibit 2. We are currently working on a methodology for handicapping sanctions risk, but because sanctions are somewhat dependent on the political landscape in developed countries (mainly the U.S. and Europe for this purpose), they will be inherently difficult to predict.

Opportunity from Default

Does the recent spate of defaults present any opportunities for us? We believe so. In Exhibit 2 we show average bond prices of selected countries that are either in default or have recently emerged from default, along with the average historical sovereign debt recovery rate calculated by Moody’s. Each of these country cases is unique, and the past average does not necessarily predict future recoveries. But as the chart shows, the majority of currently distressed countries’ bond prices are significantly lower than historical recovery value. To us, this indicates that the current level of debt distress is priced into (or perhaps more than priced into) the market. We believe this represents an opportunity for investors like us with the patience to wait for these situations to play out. In our view, this is currently one of the most attractive areas of the emerging debt asset class.

Exhibit 2: Average Bond Prices of Selected Defaulted and Debt Distressed Sovereigns

As of 2/27/2023 | Source: JP Morgan, GMO

Note: For Tunisia, yen-denominated sovereign bonds are used. For Russia, prices of bonds as currently marked in the GMO Emerging Country Debt portfolios.

Download article here.

Importantly, the vast majority of countries in our investment universe have not defaulted, and those that have were largely predictable. We triaged the debt sustainability of the sovereign debt universe in “Emerging Countries Are More Resilient Than They Get Credit For,” published in August 2022.

It is now apparent that Putin may have been shoring up Russia’s balance sheet before the invasion of Ukraine to minimize the financial cost to Russia.

Disclaimer: The views expressed are the views of Carl Ross through February 28, 2023 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2023 by GMO LLC. All rights reserved.

Importantly, the vast majority of countries in our investment universe have not defaulted, and those that have were largely predictable. We triaged the debt sustainability of the sovereign debt universe in “Emerging Countries Are More Resilient Than They Get Credit For,” published in August 2022.

It is now apparent that Putin may have been shoring up Russia’s balance sheet before the invasion of Ukraine to minimize the financial cost to Russia.