White Papers

Jeremy Grantham, Simon Harris, Ben Inker, and Catherine LeGraw sat down to provide their perspective on how investors can profit from a growth bubble. A decade of low rates and tepid growth has seen investors aggressively bid up the relative valuations of growth stocks. This intensified even further in the Covid environment and investor frenzy around fast-growing companies has catapulted them to “bubble” levels. Despite value’s recent outperformance relative to growth, the current valuation spread remains absurdly wide and provides one of the most exciting investment opportunities we have seen in decades. To exploit this growth bubble, GMO recently launched the GMO Equity Dislocation Strategy, a long value/short growth portfolio designed to balance risks while profiting from this valuation gap closing to more normal levels.

Contact Us to Watch the Replay*

*This content is intended for accredited investors only.

"The termites of doubt in 2000 attacked the stocks with the greatest level of optimism first. And they are doing almost eerily the same now. I would say on that ground, this bubble is behaving itself very well and looks like we are in the closing weeks or months of the game."

– Jeremy Grantham

Key Points

- Jeremy’s current thinking on today’s “full-fledged, epic bubble”

JG: I have heard quite a bit the argument about healthy rotation. That brings the memory of 2000. We are rotating out of super overpriced tech into cheaper stocks, so the market is getting cheaper. We are attacking first Tesla and the SPAC index, down 25% each, they are the very center of the bubble. They embody more euphoria by far than the average. People see that as healthy. But what they are missing is this: this is not about value. Value has been forgotten long ago. This is about enthusiasm, confidence, optimism. The termites of doubt in 2000 attacked the stocks with the greatest level of optimism first. And they are doing almost eerily the same now. In September 2000, having kind of finished with the slicing/dicing, they then transferred to the merely substantially overpriced broad market and the entire remaining market – 70% – rolled over like some giant iceberg and went down 50% over two years. Bubbles always peak in times of maximum confidence. That is the very nature of how these bubbles go – forget value, concentrate on overconfidence. Look for the market to attack the highest confidence first, and work its way down to the broad market, which is merely overconfident as opposed to supremely overconfident. I would say on that ground, this bubble is behaving itself very well and looks like we are in the closing weeks or months of the game.

JG: Today, it is clear to me this is the most dangerous package of overpriced assets we have ever seen in the U.S. Jim Grant would say we have the most overpriced fixed income market in the history of man. That combined with an equity market that can easily lose $5 or 10 trillion dollars depending on the magnitude of the break and is a contender for the highest priced market in American history. Housing in February hit the same price as the top of the great housing bubble of 2007. This time we are going for the trifecta: we have suddenly a housing market that is racing upwards, the euphoric equity market, and a ludicrously overpriced bond market. If they go together, they will carry a write-down in perceived wealth that would have no precedent.

- The GMO Equity Dislocation Strategy was specifically designed to profit from the view that growth stocks are in a bubble.

CL: There are many ways you can play a growth bubble. You can short growth stocks but that is a challenging way to compound wealth in the long term. You can take a long position in value stocks, but if the market melts down, you can potentially lose money even though your core thesis is correct. The absolute return nature of our Strategy is critical because we are set up to make money if our investment thesis is correct, independent of overall market performance. The Strategy is 100% long the cheapest value stocks and 100% short the most expensive growth stocks. Active security selection is a key feature of the Strategy: it reduces unrewarded risks, makes a more sophisticated and nuanced valuation assessment (some growth stocks actually deserve their valuations), and concentrates our capital in the most misvalued (and therefore highest opportunity) names. We are invested in this Strategy across our Asset Allocation portfolios but also have a Limited Partnership vehicle for investors to access this Strategy directly.

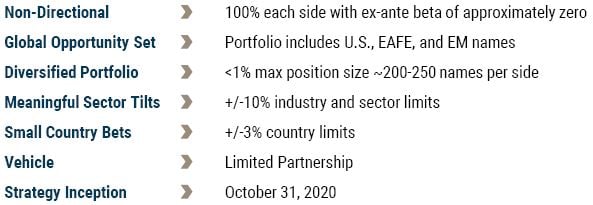

GMO EQUITY DISLOCATION STRATEGY

Absolute return strategy designed to profit from a Growth bubble

These are internal guidelines only and are subject to change without notice.

- Why launch the Strategy now? Value is extraordinarily cheap while many growth companies are showing signs of speculative excess.

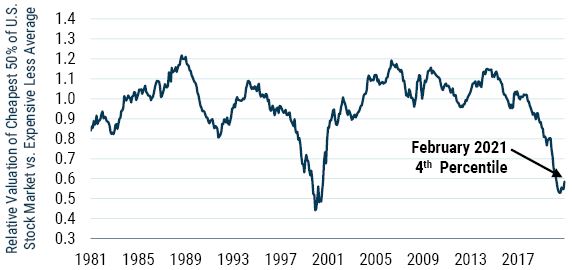

BI: This is not the first time we have launched a strategy in response to what we have seen as a real dislocation in the equity markets. We did do that in 2000 when we saw the huge dislocation between value and growth stocks. The current value opportunity is reminiscent to us of previous bubbles in global markets. It doesn’t really matter how you slice value – region, sector, size – value is extraordinarily cheap. A notable difference between today and this time a year ago is that we are also seeing “the stupid,” or the grossly speculative kind of behavior that had been the hallmark of prior bubbles. That doesn’t mean every growth stock is grossly overvalued, but what we do see is a series of such companies trading at extraordinary valuations on the back of pretty thin narratives. One of things about speculative bubbles that gives us confidence – even if we are betting the other side – is the fact that once a speculative bubble gets going, it is on limited time. There is only so long these bubbles can continue because they are kind of a naturally occurring Ponzi-like scheme. At some point when you stop being able to get more and more money in, the ability to maintain these extraordinarily high multiples just becomes impossible. We have seen a recovery in value since last October, but it’s only a small down payment on what we think is potentially available for investors. If value fully reverts to a historically normal discount, that would get you about a 70% return of value relative to growth, that is the scale of opportunity remaining for us to try to capture.

Value is Extremely Cheap

As of 2/28/21 | Source: GMO

Composite Valuation Measure is composed of price/sales, prices/gross profit, price/book, and price/economic book. Value and Growth groups are both sliced over 12 months.

- What is unique about our alpha engine? A few critical advantages over simpler value metrics.

SH: Any model that seeks out the cheapest stocks in a simplistic way will always gravitate to those with the most problems, e.g., the junkier, lower quality ones with the poorest growth prospects. We are not using any of the traditional valuation metrics to select securities for this portfolio. We at GMO have been shouting for more than two decades about the problems of the accounting numbers. Put simply, the accounting rules that we use today were put together for a different era, when an asset was a tangible item like a factory or machine and certain activities like buybacks weren’t allowed. It means that many accounting values today are at best misleading, and at worst are totally meaningless. Our Price-to-Fair-Value model (PFV) builds on years of work adjusting reported accounts to better reflect economic reality. We have built growth expectations directly into our model and are giving higher growth, less capital-intensive businesses a better chance. We are giving everyone a chance, making them look comparable across industries, countries which is much better for our valuation.

- If you find yourself today with a significant growth bias that you do not want, our Strategy is a very capital effective way to get rid of that.

We believe the GMO Equity Dislocation Strategy can enhance return and reduce risk in a diversified investment program. It can serve in a wide array of roles, including as an uncorrelated source of return in a traditional balanced portfolio, as part of a diversified hedge fund allocation, in a liquid alternatives program, or as a way to reduce the beta within a global equity allocation. The Strategy could also be used as a positive expected return hedge for a growth style equity portfolio.

BI: One reason why a number of successful investors have been quick to put money into a Strategy like this is they have somewhat inadvertently gained a very substantial growth bias to their portfolio. This comes from the venture capital they have, or their high conviction managers have tended to have a growth bias. If you find yourself today with a significant growth bias that you don’t want, our Strategy is a very capital effective way to get rid of that. In our multi-asset portfolios, where we are prepared to bet strongly on areas where we see tremendous opportunities, we have allocations to this as high as about 20% and we are comfortable with that. We see this as a very high conviction bet, a once in a decade opportunity. The size we are seeing people in their own portfolios is really a combination of two things: how much are they prepared to have a value to bias in their overall portfolio and what the rest of their portfolio looks like.

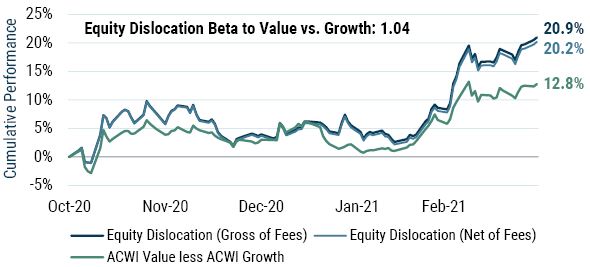

- Value Reversion has Much Further to Run – Opportunity Remains Robust Looking Forward

Our Strategy has experienced solid performance to date (20.9% total return gross of fees and 20.2% net of fees as of March 30, 2021), and we believe this is only the beginning of a major value reversion.

Equity Dislocation Strategy since launch

Data from 10/31/20 to 3/30/21

Download the Event Highlights here.

Disclaimer: Performance data quoted represents past performance and is not predictive of future performance. Gross returns are presented gross of management fees and any incentive fees if applicable. Gross returns include transaction costs, commissions, withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. If management fees were deducted performance would be lower. Net returns are presented after the deduction of a model advisory fee and a model incentive fee if applicable. Net returns include transaction costs, commissions and withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. Fees paid by accounts within the composite may be higher or lower than the model fees used. A Global Investment Performance Standards (GIPS®) compliant presentation is available by clicking the GIPS® Compliant Presentation link on GMO’s website. GIPS® is a registered trademark owned by CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

The views expressed are through the period ending March 2021, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2021 by GMO LLC. All rights reserved.