Executive Summary

In the face of the climate crisis, the world urgently needs new infrastructure for energy, transportation, and industry. The combination of depressed economic growth, rising inequality, negative real interest rates, and now the economic impact of Covid-19 makes this the most suitable time in decades for the incoming U.S. administration to launch a major fiscal program addressing this need. Such a program would help the climate, help the economy, and even be to the long-term geopolitical advantage of the U.S.

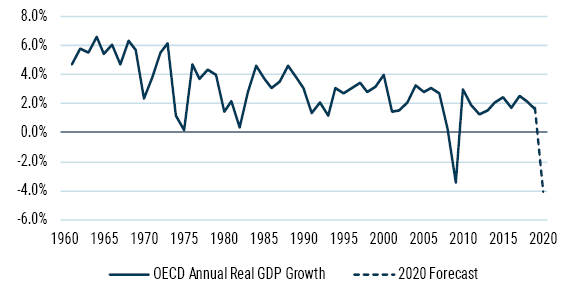

The economy of the developed world has been steadily becoming less dynamic for the last 50 years and the GDP growth of the developed world has fallen from over four percent a year to less than two percent a year (see Exhibit 1). Even this slower pace of growth is threatened by longer-run problems from climate change and shorter-run problems from Covid-19 – which has tentacles reaching into 2022, and far beyond for some economic subsets. Work from home changes are hard to call, but at worst they may crush commercial property prices and quite possibly city apartment prices too.

EXHIBIT 1: DEVELOPED WORLD ANNUAL REAL GDP GROWTH

As of: 10/27/20 | Source: World Bank, OECD

Of these problems it is the longer-term malaise that worries me most. I believe income inequality is eating away at the economy from the inside with the lack of economic progress for workers reducing demand. In the U.S. that is covered up temporarily to some extent by the short-term explosion of a small set of new disruptive FAANG-type companies.

This however is where a magic bullet comes in: we need a long, sustained and massive public works program – a second coming of the Marshall Plan, if you will – to jolt the U.S. and the global economy into a few decades of accelerated growth. The trouble here is that much of the world has lost heart after the financial crash because it is unnecessarily concerned with debt levels.

I have always believed that the significance of debt is greatly exaggerated. It is double-entry bookkeeping. For every dollar owed there is a creditor to whom it is owed. And if you are concerned with liquidity, then of course it is interest coverage that counts and today’s negative real interest rates for risk-free loans, even on long dated debt, makes it a very advantageous time for governments and corporations to borrow and invest. Yet many of them act as if they are intimidated by the debt ratio, as opposed to interest coverage.

Now we face the shorter-term economic threat from Covid-19 and the long-term economic threat from climate change (although suddenly its short-term impact from fires and floods is also getting to be painful). We have a clear incentive, I would argue an imperative, to produce a very large and sustained public works program.

The great waste in 2009 and 2010 in the U.S. was the use of precious resources to bail out banks, including those who had made large commercial bets and lost. They were not simply illiquid as in a classic “run on the bank”: they were insolvent. Bailing them out was both unjust and economically inefficient; it was a violation of the spirit of capitalism. This time we need to have infrastructure dominate the program.

And what better time to do this than now for two reasons. First, in the U.S. our current infrastructure is unusually behind schedule on maintenance and subpar in quality. Second, it is absolutely imperative that the entire economy be greened if we want any hope to maintain a stable global civilization in coming centuries. This will take tens of trillions of dollars, over several decades, on a global basis. The good news is that infrastructure spending, particularly green infrastructure spending, pays a respectable return on investment as far as the eye can see. If financed at negative real rates, it is the commercial bargain of all time. Even if it crowds out some ordinary commercial activities on the margin, it is still a bargain, for little of routine GDP shows a long-term societal return. And given currently depressed demand, the crowding-out effect should be small.

A program modeled on the Marshall Plan would help address growing inequality. Typical workers – as we are all beginning to realize – have been hung out to dry, really since the mid-1970s. Much of the spending on new infrastructure would be industrial and labor-intensive. It would have the same effect as a major onshoring of manufacturing, providing hundreds of thousands of jobs and raising wages for both skilled and unskilled labor. (Although, certainly, retraining and improving skills will remain a priority given the changing economy.)

It would also help challenge the growing dominance of China in the energy and industrial technologies of the next century. Under current trends, that dominance could soon become unassailable. For one example, the U.S. has 400 electric buses, while China has 400,000! Green energy and industry will be not just economically important in coming decades, but, like oil was before, incredibly geopolitically important. A major new infrastructure program would help the U.S. – still the most innovative country in the world – catch up to China's lead.

You get the point. Not only does green infrastructure produce a good return, jolt the economy forward, and help with inequality, it also helps create an environment where the U.S. can at least fight it out with China for leadership in what will become the dominant industries of 2050. And, above all, it will insure against the staggering costs of a failure to control our climate, which at worst will be incalculable – the disintegration of a reasonably stable global society. So now is the time. Bring it on.

Download article here.