Executive Summary

While the passive balanced portfolio (60% stock/40% bond) has outperformed more diversified allocations over the last decade, we believe investors should temper their expectations for a repeat. Two key problems lie ahead for such a portfolio. First, stock and bond valuations are both extended, suggesting they will deliver less than they have historically. Second, the duration of a 60/40 portfolio is near its apex with both stocks and bonds exposed to future changes in discount and interest rates. Even a small rise in the aggregate yield of the 60/40 would impair returns. There is simply less underlying yield to cushion capital losses, which would be larger than normal given today’s high duration. Liquid Alternatives can help mitigate these dual threats given their low durations and diversification benefits.

A passively allocated 60% stock/40% bond portfolio has well served investors seeking to compound wealth with reasonable levels of risk. A global 60/40 portfolio1 delivered 7.3% after-inflation returns from the lows during the Global Financial Crisis through 2019. A U.S.-biased balanced portfolio2 did even better, chalking up annualized real returns of 9.5% – more than double the long-term average of 4.4% going back to 1900. While the passive balanced portfolio has delivered extraordinary recent returns and can be easily and cheaply implemented, investors should be wary looking forward. Two key problems lie ahead.

Problem #1: Low Yields from both Stocks and Bonds

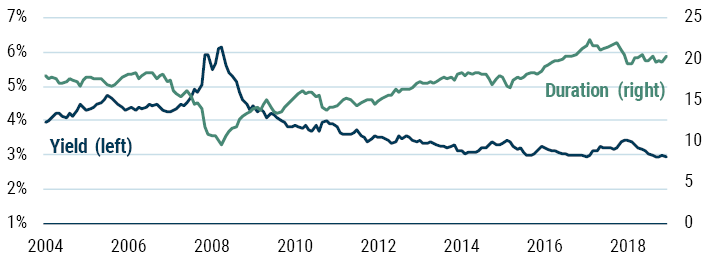

First, stock and bond valuations are both extended, suggesting they will deliver less than they have historically. The math with bonds is straightforward. 10-Year U.S. Treasuries yielded just under 2% at the end of 2019 and even less today. It is more or less impossible for a bond index yielding roughly 2%3 to deliver the 5% nominal returns investors have become accustomed to over any period of time approaching or exceeding the index’s duration. Of course, anything (including even lower rates) can happen in the short run. Similarly, the underlying earnings yield of the stock market has fallen as valuations have risen. The blue line in Exhibit 1 traces the aggregate yield of a 60/40 portfolio by combining the normalized earnings yield for stocks (S&P 500) and the yield-to-worst for the Bloomberg Barclays U.S. Aggregate Bond Index. Unless expensive valuations rise higher and low rates fall lower, the passive 60/40 portfolio will likely deliver disappointing returns. The low starting yield of a 60/40 portfolio represents the first problem we see ahead.

Exhibit 1: The passive 60/40 portfolio looks unsatisfying

Source: GMO | As of 12/31/19

Shiller CAPE used to calculate both the implied earnings yield and to represent equity duration. 60/40 yield = 60% inverse of Shiller CAPE ratio and 40% Bloomberg Barclays U.S. Aggregate Yield-to-Worst. Duration = 60% CAPE and 40% Bloomberg Barclays U.S. Aggregate Duration.

Problem #2: High Duration of both Stocks and Bonds

At the same time the underlying yield is at its low point, the duration (green line) of the portfolio is near its apex. Duration measures the sensitivity of the portfolio to a change in that underlying yield. Today, the sensitivity of a 60/40 portfolio to a change in yield is nearly as high as it has ever been. Both stocks and bonds are levered to future changes in discount and interest rates. Even a small amount of mean reversion upward in the aggregate yield of the 60/40 portfolio will be painful because there is less underlying yield to cushion any capital losses and those capital losses should be expected to be larger than normal for any change in yield given the high duration. While investors have become conditioned to believe that a 60/40 portfolio delivers consistently strong returns, history shows this has not always been the case and the twin problems weighing on such a construction today suggest robust returns are unlikely going forward. Due to elevated valuations (low yields) and extended durations of both stocks and bonds, it is possible that in a future downturn investors will not receive the diversification they expect from their bond portfolio. Stocks and bonds have risen together and could certainly fall in unison as well.

Liquid Alternatives Offer a Potential Solution

To address these dual threats, we have rotated into risk-controlled, highly liquid alternative strategies across our multi-asset portfolios. These strategies take risks in ways that provide very low durations, offering an important form of portfolio diversification. For example, compare merger arbitrage to long equity holdings. With equites, you are buying a stream of cash flows stretching decades into the future. The main risks are that a depression will meaningfully impair those cash flows or that discount rates will rise and lower the present value of those long-dated cash flows. With a merger position, you are still invested in equities, but the key risk you are underwriting is the odds of that deal blowing up. Typically, transactions close or break within 12 months, leading to a significantly shorter duration profile than traditional equities.4

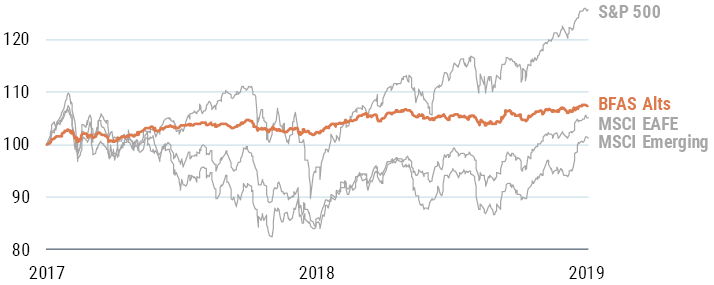

Liquid Alternatives can provide diversifying and uncorrelated returns. While Alternatives should not be expected to keep up with robust equity markets, they can help shield large drawdowns given their lower equity beta exposure. GMO’s suite of Alternatives within our Benchmark-Free Allocation Strategy has delivered generally in line with our expectations through the volatility of the last couple of years as Exhibit 2 indicates. Liquid alternatives improve the robustness of our multi-asset portfolios by helping to protect against the problems that today’s low yields and high durations present.

Exhibit 2: ALTS – MARCHING TO THEIR OWN DRUMMER

As of 12/31/19 | Source: GMO

*Gross of fee returns.

Past performance is no guarantee of future results.The above information is based on a representative account in the Strategy selected because it has the fewest restrictions and best represents the implementation of the Strategy.

Download article here.