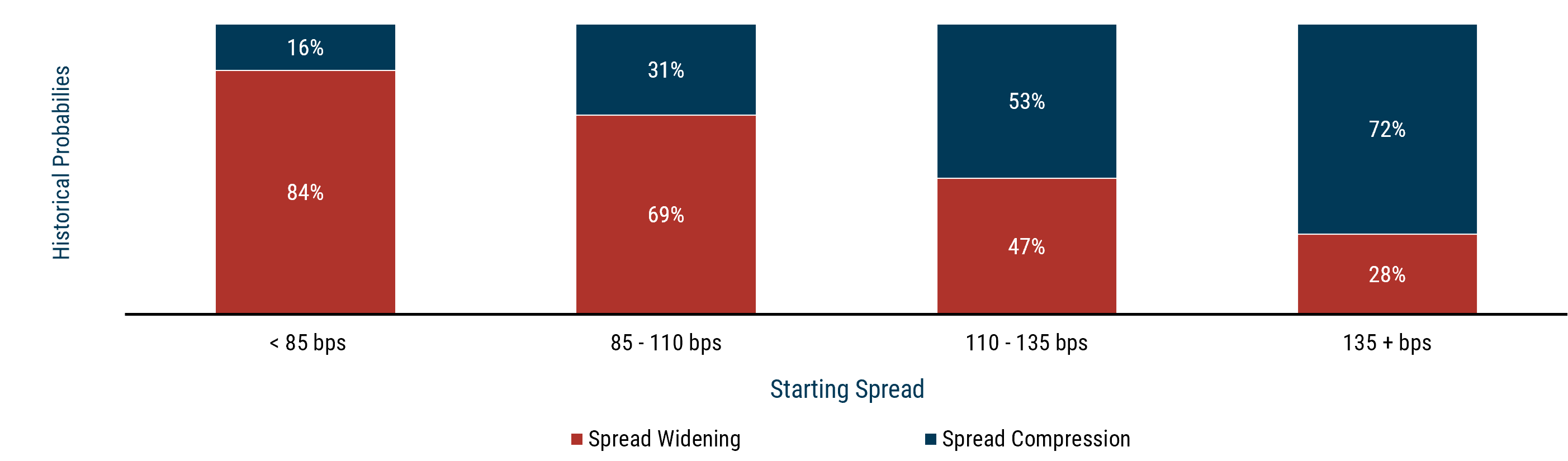

Investment-grade (IG) corporate bond 1 spreads are hovering inside 85 basis points, placing them near the 19th percentile over the past five years. At these levels, valuations are stretched, leaving investors with little potential upside and increased vulnerability to spread widening. In our view, such an environment warrants a shift toward high-quality assets.

Historical data since 1998 suggests that the potential for further spread tightening from here is extremely limited. Indeed, given starting spread levels inside 85 bps, our analysis revealed an 84% probability of spread widening over a 1-year horizon. IG spreads need to be significantly wider (in the 110 to 135 bps range) than they are now before they’ll offer a more balanced risk profile (or 47% probability of spread widening). Yet, the instinct to reach for yield persists in the market today, tempting many investors to accept ever-thinner compensation for credit risk.

EXHIBIT 1: INVESTMENT-GRADE CORPORATE BONDS

Probabilities of 1-year forward spread changes, conditioned on starting spread

Data for the period Jan 1998 - Mar 2026 | Source: Bloomberg, GMO

In this environment of very limited upside, we think that a conservative posture and a shift toward quality is prudent. Some investors may argue that IG corporates offer an appropriate quality tilt because of their low probability of principal loss. While we agree that IG corporate default risk is quite low, the potential for negative mark-to-market price risk over some reasonable holding period is not. And high-quality structured credit, in our opinion, enables an investor to both avoid the risk of principal loss and significantly reduce material downside mark-to-market price risk brought about by spread widening. As we argued extensively in our August 2025 publication, Structured Credit: A Better Margin of Safety When Spreads Are Tight, the mark-to-market risk for certain sectors with longer maturities (i.e., spread duration) like U.S. IG can be very one-sided and negative, overwhelming the average expected spread over a comparable risk-free rate over some shorter holding period. This dynamic, fortunately, is present to a much lesser degree within our structured credit strategies—where spread durations are significantly lower.

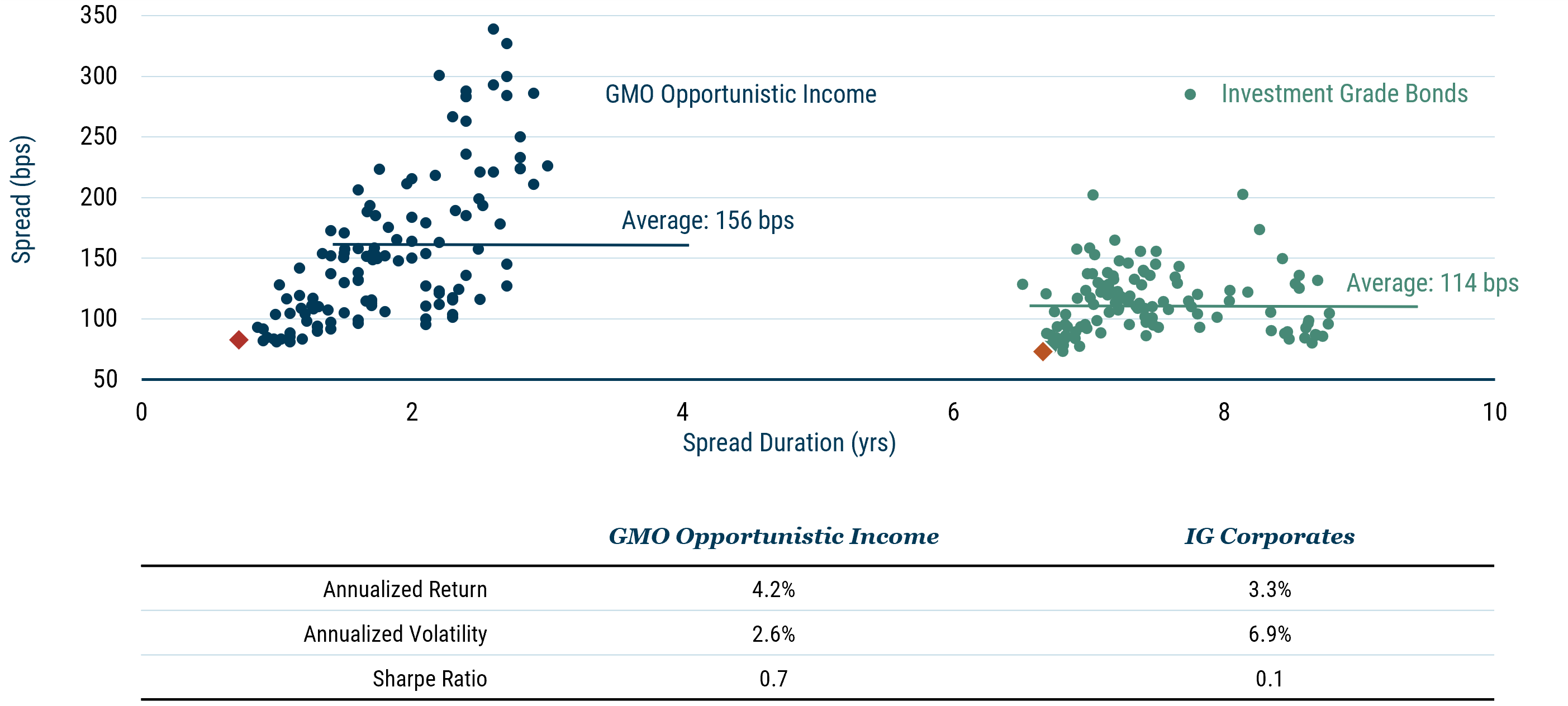

Lower spread duration naturally reduces price volatility, but in managing our structured credit portfolio, the GMO Opportunistic Income Strategy, we seek to go beyond merely minimizing spread duration risk when spreads are at historically tight levels. Let us expand here on two often underappreciated features of our structured credit strategy that help us mitigate downside risk during periods of market volatility. The first is our focus on the senior part of the capital structure—we find that the market rarely compensates investors enough to go down in credit, especially in bull markets. The second is how we avoid negatively convex profiles, which further enhances the quality of our strategy. Prioritizing these quality features has helped ensure return resiliency through the credit cycle. As a result, our strategy has consistently delivered high-quality carry or, in other words, an average spread advantage over IG of 42 bps with 5.6 years less duration on average since 2016 (Exhibit 2). Furthermore, as the data shows, our willingness to tilt the portfolio toward higher-spread carry, while actively managing spread duration to minimize mark-to-market risk, has resulted in more resilient returns and a higher Sharpe ratio.

EXHIBIT 2: GMO’S ADVANTAGE—HIGHER CARRY, LESS SPREAD SENSITIVITY

Our strategy has held a consistent, higher-quality carry premium vs. IG since 2016

Data for the period Jan 2016 - Jan 2026 | Source: Bloomberg, GMO

To further illustrate how we construct a high-quality carry portfolio, let’s take a closer look at the two features that underpin our approach.

Quality Feature #1

Investors are often undercompensated for taking on structural leverage risk.

We believe that the highest risk-adjusted returns often come from the safest, most senior bond in the capital structure for two reasons. First, investors are often tempted to reach for yield in the lower parts of the capital structure, especially in a tight spread environment. This leaves the lower-yielding top of the capital structure undervalued from a risk-adjusted return perspective. Second, the most senior part of a structured product’s capital structure is by far the largest. This means it can generally trade at a lower price than smaller mezzanine tranches, which can be bid up due to scarcity value.

Senior bonds (e.g., AAA) sit at the top of the capital structure, receive payments first, and only absorb losses after the mezzanine bonds below have been written down. Mezzanine bonds get principal payments only after the senior bonds are paid off, but take losses first. For example, in a standard CMBS multi-borrower deal, a AAA-bond is the “30-100 slice,” which means this bond won’t take a principal write-down until the cumulative losses in the underlying collateral exceed 30%. Even then, a 1% increase in losses (from 30% to 31%) reduces the bond’s face value by only 1/70th. We refer to this type of bond as having low structural leverage.

Conversely, a BBB-rated bond in these structures is the 7-9 slice in the deal and will start losing principal once collateral losses reach only 7%. A move from 7% to 8% wipes out 50% of the bond’s face value. Once losses reach 9%, the bond is completely wiped out, and investors recover no principal. We refer to this type of bond as having high structural leverage.

We generally prefer senior, thicker tranches because they offer better risk-adjusted returns than thin mezzanine slices. We don’t think investors require enough compensation for taking on structural leverage risk, which drives down the cost of quality in the higher parts of the capital stack. Several factors might play a role in this, including the fact that many investors face investment-grade rating constraints but are unconstrained within the IG ratings subset. This often causes them to reach for yield by buying lower IG-rated bonds (A or BBB), even when the compensation for the higher structural leverage is insufficient. This behavior intensifies when spreads are tight and yield targets are hard to meet.

At GMO, we only go down in credit when we feel very strongly about the quality of the collateral and believe we are adequately compensated for the added risks referenced above.

Quality Feature #2:

Avoiding negative convexity when not properly priced improves a portfolio’s return profile.

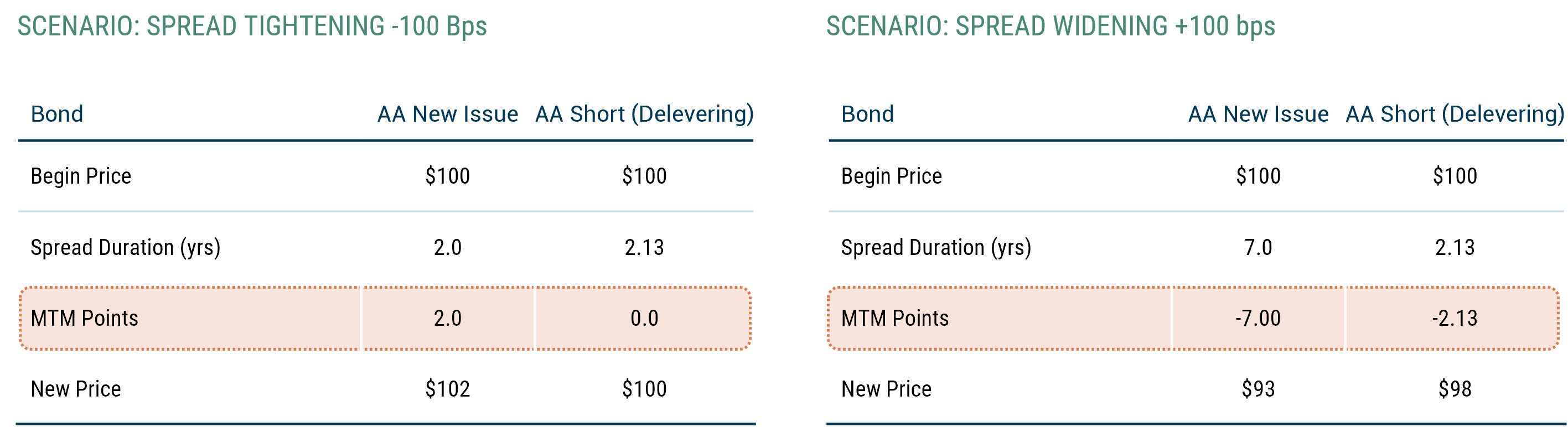

We define negative convexity as the feature where certain bonds (e.g., CLOs, CMBS SASB floaters) may behave in a manner contrary to investor expectations because the borrowers or issuers (or both) have an embedded option to prepay the loans or the security in question. In other words, when credit spreads or yields tighten, the spread duration or rate duration of these securities usually falls in tandem, muting the benefit of further tightening. At the same time, when spreads or rates sell off, duration extends, magnifying the investor’s mark-to-market pain. Given its distinct callability feature, the CLO sector of the structured product market exemplifies the impact of negative convexity. In this well-bid market environment, when bonds trade at par or even at a small premium, the value of the borrower’s embedded call option goes up significantly. If spreads tighten, borrowers have a greater incentive to call or refinance the bond at par. Meanwhile, if spreads widen, the borrower will likely do everything he or she can to extend the transaction by reinvesting prepayment proceeds to the full extent allowed by the prospectus. This extension magnifies the effect of the spread widening. The benefits to the borrowers are asymmetric to those of the capital lenders, whose capital gains from potential price appreciation are limited to the call price, usually at par.

Let’s compare a full-duration, new-issue AA-rated CLO to a seasoned AA-rated CLO that has exited its reinvestment period and therefore has a much shorter duration. The typical structure for CLO transactions is a 2-year non-call period followed by a 4-year reinvestment period. As a result, the new-issue AA CLO bond will remain outstanding for at least two years, but under certain conditions, its maturity can extend to roughly seven years. In contrast, a seasoned AA-rated CLO that is out of reinvestment will soon begin to amortize. It can be called immediately, and even if the manager reinvests prepayments to the maximum extent allowed by the prospectus, the bond will likely remain outstanding for no more than around two years.

From a performance standpoint, starting at par ($100), a AA-rated new-issue CLO with two years of spread duration may see a 2% mark-to-market gain if spreads tighten by 100 bps. The seasoned, shorter-duration AA CLO bond, however, would likely be called immediately, capturing no upside. On the downside, if spreads widen by 100 bps, the new-issue AA-rated CLO may extend to seven years of spread duration, resulting in an approximately 7% mark-to-market loss compared to an only 2.1% loss for the seasoned, shorter-duration AA-rated CLO.

EXHIBIT 3: Avoid negative convexity

Source: Intex, GMO

Given the risks are skewed to the downside and the market is currently very well bid, we think owning the shorter-duration, de-levering CLO is the more compelling choice: it limits the potential price downside of the more negatively convex longer securities and provides a better margin of safety.

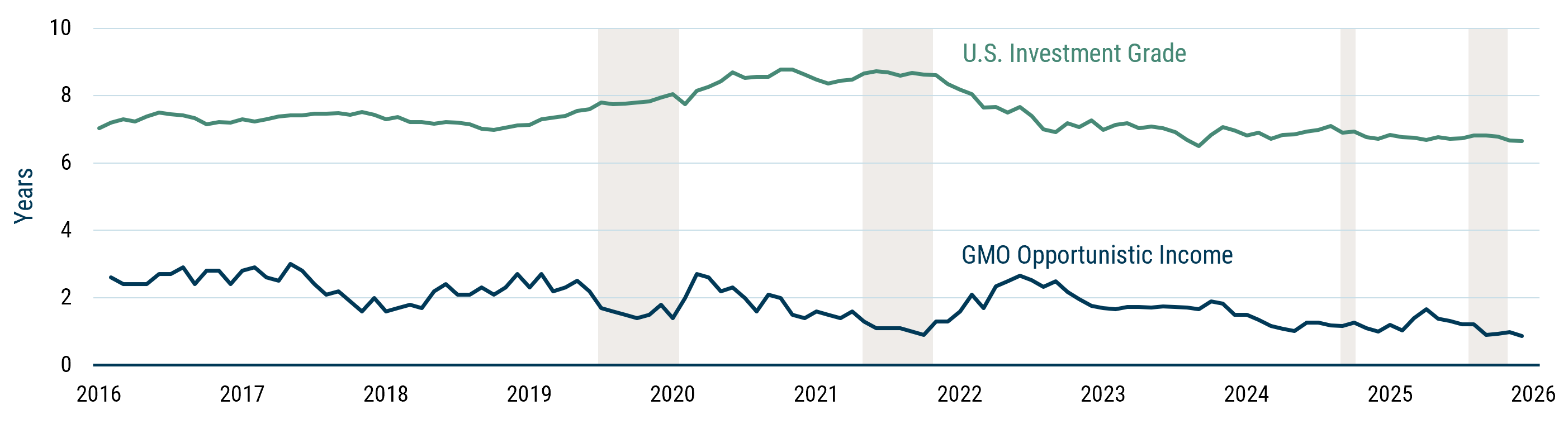

Our investment process has steered us toward reducing spread risk in the portfolio at various market inflection points, as it did at the end of 2019 and 2021, at the end of 2024 and early 2025, and going into 2026.

EXHIBIT 4: Spread Duration

As of 1/31/2026 | Source: GMO

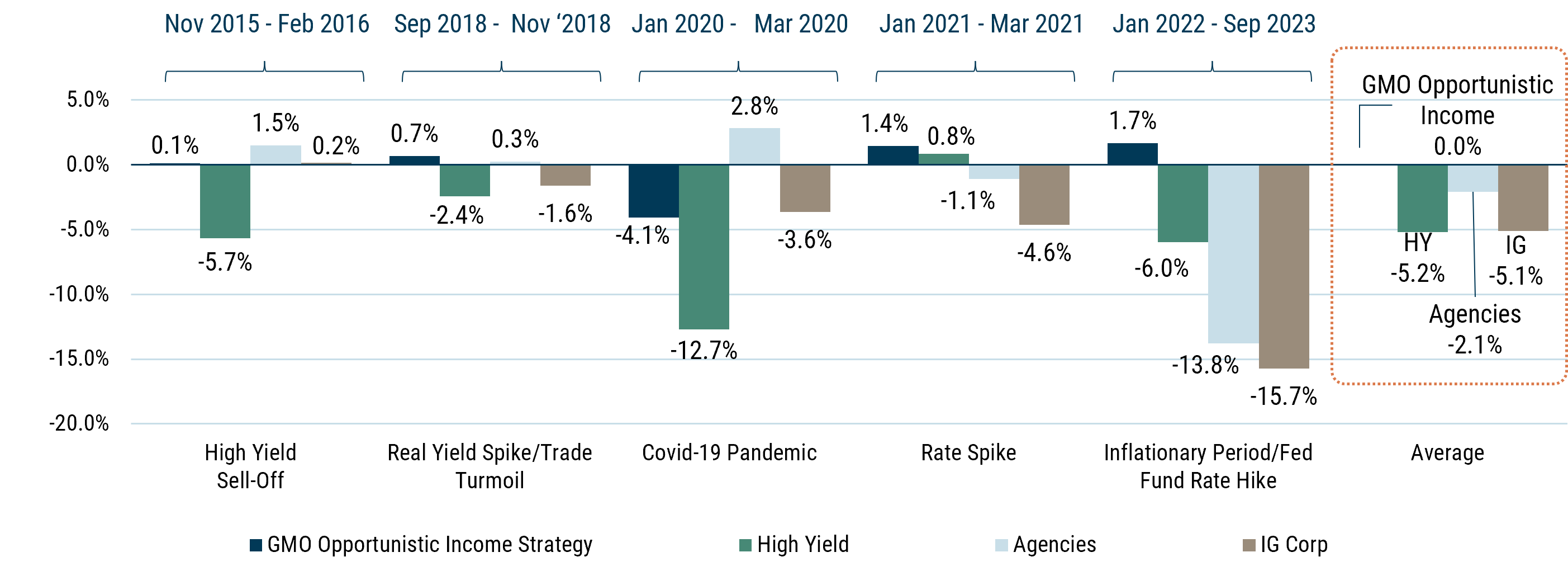

This conservative stance helped us weather the high-yield sell-off of 2015-2016, the real-yield spike of 2018, the pandemic of 2020, the rate spike of 2021, and the inflationary period and federal funds rate hike of 2022-2023. In particular, the high-yield sell-off, (triggered by weakness in energy, metals, and mining) and the Covid-19 pandemic were the two credit-related events where quality feature #1—lower structural leverage—resulted in better downside protection. In the other three instances, quality feature #2—avoiding negative convexity—buoyed returns. As Exhibit 5 shows, our high-quality carry portfolio has not outperformed in every major adverse market event over the past decade; however, it has fared better on average than agency MBS, where negative convexity is particularly pronounced, and corporate credit.

EXHIBIT 5: HIGH-QUALITY CARRY RESILIENCE IN MAJOR MARKET DOWNTURNS

Source: GMO

In today’s uncertain environment, characterized by frothy valuations in many segments of the market, we believe the risk/reward trade-off in structured credit is more favorable. While many investors buying IG bonds are primarily focused on yield (not spread), most investors cannot afford to ignore the mark-to-market risk associated with potential spread widening. In this context, an actively managed structured credit exposure with a high-quality tilt offers the advantage of a higher spread break-even compared to U.S. IG, thereby increasing the likelihood of outperformance relative to a comparable risk-free investment. Even if spreads remain at current levels, GMO’s Opportunistic Income Strategy offers superior all-in carry compared to U.S. IG, supported by both spread and yield advantages.

We approximate investment-grade (IG) bonds with the Bloomberg U.S. Corporate Bond Index.

Disclaimer: The views expressed are the views of Joe Auth, Ben Nabet, and Mina Tomovska through the period ending March 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2026 by GMO LLC. All rights reserved.

We approximate investment-grade (IG) bonds with the Bloomberg U.S. Corporate Bond Index.