Insights

Listen to this Insight

Key Takeaways

- Today’s traditional stock and bond portfolios 1 are highly exposed to a small set of shared macro risks, increasing the likelihood of synchronized drawdowns.

- In an environment of high equity valuations, tight credit spreads, and elevated macro uncertainty, stock and bond portfolios are especially vulnerable to these risks.

- In this context, liquid alternatives may offer one of the few scalable ways to pursue diversification within more liquid investment vehicles, making them attractive as both a strategic allocation and a tactical overweight.

- GMO’s Alternative Allocation Fund (ALTA) is a U.S. mutual fund (ticker: GAAGX) that seeks to generate a return stream that is uncorrelated to traditional equity or fixed income indices in a daily liquid mutual fund structure with a single management fee.

- ALTA employs a carefully balanced, multi‑strategy approach, providing diversified exposure across numerous return drivers and alpha engines.

The logic of balanced investing is straightforward: equities drive long-term growth, bonds provide income and ballast when stocks fall, and the combination delivers a smoother ride than either asset alone. For decades, the 60/40 portfolio has been the default framework for good reason – it has worked, often brilliantly, across multiple market cycles.

What has changed is not the logic of diversification, but the reliability of its traditional building blocks. In recent years, the correlation between equities and bonds has risen materially. In 2022, equities and bonds declined simultaneously, leaving balanced portfolios with nowhere to hide. More recently, in March 2026, the war in Iran and the closure of the Strait of Hormuz triggered an oil supply shock, in which a traditional 60/40 portfolio lost roughly 5% in a single month. These episodes were relatively short-lived, yet history shows that stock/bond correlation can remain positive for extended periods, eroding diversification precisely when investors need it most.

S&P500–BLOOMBERG U.S. AGGREGATE ROLLING 2-YEAR CORRELATION

As of 3/31/2026 | Source: GMO

Both equities and credit are currently trading at stretched valuations, compounding the problem. High market concentration, rising inflation, disruption from AI, central bank balance sheet expansion, and the growing risk of stagflation all present asymmetric threats to traditional stock and bond exposures. In this environment, liquid alternatives have the potential to serve as one of the few safe havens for investors if we experience a major market correction.

Not All Alternatives Are Truly Diversifying

Many investors have increased allocations to alternatives in search of better diversification and higher returns, including sizeable allocations to private equity and private credit. The appeal is understandable. Historically, these asset classes were touted for their potential to deliver strong absolute returns that appeared uncorrelated to public markets. Yet, much of that apparent diversification reflects illiquidity and appraisal-based pricing rather than genuinely different underlying risk exposures.

A leveraged buyout fund and a public equity portfolio are both fundamentally exposed to corporate earnings growth and credit conditions. When those macro factors deteriorate, private and public assets suffer in tandem; private portfolios simply report the damage with a lag. Smoothed returns should not be confused with diversified returns.

This distinction matters in practice. If the goal is to build a portfolio that is genuinely resilient across a wide range of economic environments – rather than one that merely appears stable on quarterly statements – investors need to look beyond how asset classes are packaged and instead focus on return drivers that are fundamentally different in nature.

Liquid Alternatives Offer Diversifying Returns and Portfolio Flexibility

Liquid alternative strategies were designed to address this problem by expanding the opportunity set. Unlike traditional long-only investments, which largely represent directional exposure to economic growth, falling rates, or tightening credit spreads, liquid alternative/hedge fund strategies draw returns from sources that are structurally distinct from the equity and bond risks that dominate most portfolios. Broadly, these strategies fall into two categories.

The first category, alternative risk premia (ARP), harvests returns rooted in market structure and investor behavior. They compensate investors for bearing risks that are uncomfortable or difficult for most market participants to hold consistently.

- Merger arbitrage is a classic example. It earns a spread for bearing the risk that announced deals may fail to close.

- Carry strategies systematically harvest yield differentials across currencies, rates, or commodity futures curves.

- Volatility selling earns a premium from market participants willing to pay for insurance against abrupt market moves.

- Trend-following captures the well-documented tendency for assets in motion to stay in motion, driven by underreaction, herding, and delayed information diffusion.

Each of these premia has a clear economic rationale for why it exists, why it persists, and why it behaves differently from traditional equity and bond returns. These strategies generally have a positive expected return across market environments and can provide a persistent source of returns to portfolios. However, ARP tend to experience near-term losses during market shocks due to deleveraging or a flight to safety. Skilled managers aim to add alpha on top of these premia through careful design and differentiated implementation.

The second category – alpha strategies – generate returns through relative mispricings, fundamental security selection, and event-driven catalysts. Returns from these strategies are driven by manager skill rather than beta or directional exposure. As a result, they tend to behave idiosyncratically during periods of market stress, with outcomes shaped more by portfolio positioning and the nature of the shock than by broad market direction.

When combined, alternative risk premia and alpha strategies reduce reliance on the narrow set of macro risk factors that drive stocks and bonds, which can help stabilize potential outcomes across a range of market regimes.

Liquidity is a Strategic Advantage

Beyond the return characteristics, we believe there is another dimension of liquid alternatives that is often underappreciated: liquidity itself is a strategic advantage, not an operational detail.

When risk assets sell off sharply, precisely the moment when forward return opportunities improve, illiquid investments such as private equity and private credit are harder to rotate out of and into cheaper risk assets or be used to fund spending needs. If liquidity is required, investors are often forced to sell underperforming (public) equities or bonds at the worst possible time.

Alternatives with daily liquidity seek to avoid these constraints. They were designed to allow investors to rebalance efficiently, respond to changing conditions, and maintain flexibility without structural impediments. In an environment where shocks can arrive without warning, we view flexibility not as a convenience – but as an essential.

GMO Alternative Allocation: Designed to Deliver a Structured Approach to Liquid Alternatives

The GMO Alternative Allocation Fund (ALTA) is explicitly designed around these principles. Managed by GMO's Asset Allocation team – bringing over 25 years of experience constructing hedge fund and liquid alternative solutions – ALTA is a multi-strategy portfolio that invests across a broad spectrum of alternative strategies spanning equities, fixed income, currencies, and commodities.

Structured as a 40 Act mutual fund, ALTA offers daily liquidity. It targets returns of cash plus 4% per annum, with expected volatility of 4% to 12%. Crucially, ALTA aims to generate these returns while maintaining low correlation to traditional risk assets. 2

In our view, what distinguishes ALTA from many liquid alternatives products is the deliberate balance and breadth of its approach. The portfolio is not reliant on any single alpha source to meet its return objective. Instead, it invests in a diversified basket of hedge fund strategies – both pure alpha portfolios and strategies rooted in ARP yet implemented with meaningful manager discretion. Each strategy targets different return drivers with different approaches across multiple asset classes.

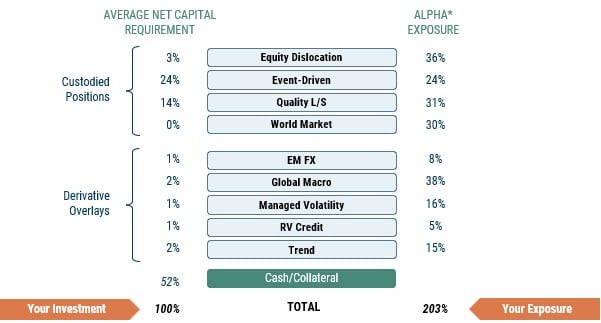

Diversified across return drivers and Asset classes

As of 3/31/2026 | Source: GMO

The Fund pursues its exposure to styles and asset groups through the underlying strategies listed above.

They all draw on the thought leadership, independent research, and investment expertise of professionals throughout GMO. By combining a diversified basket of ARP strategies that aim to deliver a reliably consistent source of returns with the more idiosyncratic returns of alpha strategies, ALTA seeks to provide positive uncorrelated returns, robust to multiple market regimes.

ALTA also benefits from significant capital efficiency. Unlike a fund-of-funds model, where each strategy sits in its own vehicle with its own cash drag and fee layer, ALTA is implemented as a single integrated portfolio with a unified pool of capital. Long and short equity positions collateralize one another, and derivative overlays provide economic exposure with low collateral requirements. This structure gains significantly more exposure to alpha per dollar invested than traditional multi-manager approaches or build-it-yourself models.

Capital efficiency

$2 of exposure for every $1 invested

As of 3/31/2026 | Source: GMO

*Alpha (α) is a measure of an investment’s excess return relative to a benchmark or market index, after adjusting for risk. It reflects the portion of performance attributable to a strategy’s design, implementation, or to a manager's skill, rather than to market movements alone

ALTA's fee structure compounds this advantage over time. Many alternative investment products embed multiple layers of fees: management fees, incentive fees, passthrough costs, and hidden expenses. ALTA charges a transparent, flat management fee with no performance fee, no high-water mark, 3 and no passthrough fees layered through a multi-manager structure. As a daily-priced mutual fund, it also ensures access to liquidity when needed most.

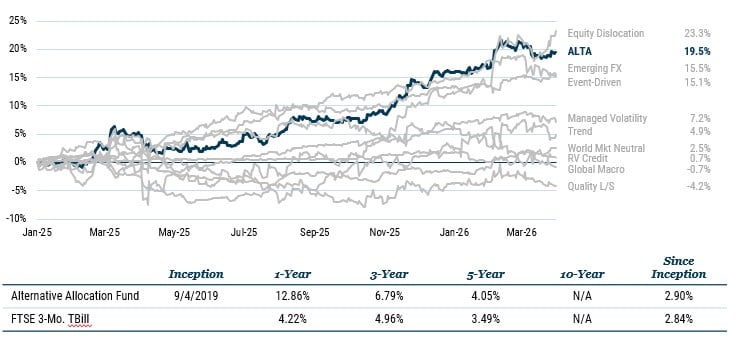

Early Results Support the Framework

Since material enhancements were made to the strategy in February 2025, ALTA has delivered results consistent with its objectives across a range of market conditions. The fund returned 15.1% net of fees for the full year 2025, significantly exceeding its cash plus 4% target, while maintaining low correlation and near-zero beta across all major risk asset classes.

During the first quarter of 2026 – amid rising concerns around AI disruption and the sharp rotation following the outbreak of war in Iran - ALTA returned 3.3% net of fees, while the MSCI ACWI lost 3.2% and a traditional 60/40 portfolio 4 declined 1.7%. In the month of March, ALTA declined 68 basis points compared to a loss of 5% for a 60/40 portfolio.

These outcomes – positive absolute performance, low correlation, resilience during stress, and balanced contribution across multiple return drivers – are exactly what the strategy is designed to deliver. For investors reassessing portfolio resilience in today’s environment, we believe ALTA merits serious consideration.

Alternative allocation strategy

Cumulative Performance

As of 3/31/2026 | Source: GMO

Returns shown for periods greater than one year are on an annualized basis. If certain expenses were not reimbursed, performance would be lower. Transaction costs, if any, are paid to the fund to offset the cost of portfolio transactions to invest or raise cash.

1

“Traditional stock‑and‑bond portfolios” refers to portfolios invested primarily in long‑only public equities and investment‑grade fixed income and does not include alternative investments (e.g., hedge fund strategies, private investments, or derivatives‑based alternative strategies).

2

The Fund at times may have substantial exposure to a single Style, asset class, sector, country, region, issuer, or currency and companies with similar market capitalizations.

3

A “high-water mark” is a feature associated with performance (incentive) fees generally charged only on new net gains after the investment’s value rises above its previous highest level (after fees). If the investment declines, the value typically must recover above that prior peak before a performance fee may be charged again.

4

A “traditional 60/40 portfolio” generally means a mix of publicly traded stocks and bonds, with roughly 60% stocks and 40% bonds. It does not include alternative investments such as hedge fund strategies, private investments, or derivatives‑based alternative strategies.

Performance data quoted represents past performance and is not indicative of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance data may be lower or higher than the performance data provided herein. To obtain performance information to the most recent month-end, visit www.gmo.com. The portfolio is actively managed, is not managed relative to a benchmark and uses the Index for performance comparison purposes only and, where applicable, to compute a performance fee. The performance information for all periods prior to January 31, 2025, was achieved prior to the change in the Fund’s investment objective and principal investment strategies.

Risks associated with investing in the Fund may include: (1) Management and Operational Risk: the risk that GMO's investment techniques will fail to produce desired results, including annualized returns and annualized volatility; (2) Derivatives and Short Sales Risk: the use of derivatives involves the risk that their value may not change as expected relative to changes in the value of the underlying assets, pools of assets, rates, currencies or indices. Derivatives also present other risks, including market risk, illiquidity risk, currency risk, credit risk, and counterparty risk; and (3) Leveraging Risk: the use derivatives and securities lending creates leverage. Leverage increases the Funds losses when the value of its investments (including derivatives) declines. For a more complete discussion of these and other risks, please consult the Fund's Prospectus.

Net Expense Ratio of 2.29% reflects the reduction of expenses from fee reimbursements. The fee reimbursements will continue until at least 30 June 2026. Elimination of this reimbursement will result in higher fees and lower performance.

Gross Expense Ratio of 2.59% is equal to the Funds Total Annual Operating Expenses set forth in the Funds most recent prospectus dated 30 June 2025.

Adjusted expense ratio of 1.15% excludes certain investment-related costs, such as dividend and interest expense on short sales and interest expense incurred through entering into reverse repurchase agreements. The total of these costs, where applicable, can be found in the most recent prospectus.

An investor should carefully consider the fund’s investment objectives, risks, charges and expenses before investing. This and other important information can be found in the fund’s prospectus. To obtain a prospectus please visit www.gmo.com. Read the prospectus or summary prospectus carefully before investing.

The S&P 500 Index is a widely followed index that measures the performance of approximately 500 large U.S. public companies and covers approximately 80% of available market capitalization. It is a market-value-weighted index (stock price multiplied by number of shares outstanding), with each stock’s weight in the Index proportionate to its market value. The “500” is one of the most widely used benchmarks of U.S. equity performance.

The Bloomberg U.S. Aggregate Bond Index is a broad benchmark that measures the performance of the U.S. investment-grade, U.S. dollar-denominated taxable bond market and generally includes U.S. Treasuries, government-related and corporate bonds, and securitized bonds such as mortgage - and asset-backed securities.

The MSCI All Country World Index (ACWI) is a global equity index that tracks large- and mid-cap stocks across developed and emerging markets, covering approximately 85% of the global investable equity market.

Indices are unmanaged, and investors cannot invest directly in an index.

The GMO Trust funds are distributed in the United States by Funds Distributor LLC. GMO and Funds Distributor LLC are not affiliated.

Disclaimer: The views expressed are the views of B.J. Brannan through the period ending May 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2026 by GMO LLC. All rights reserved.

1

“Traditional stock‑and‑bond portfolios” refers to portfolios invested primarily in long‑only public equities and investment‑grade fixed income and does not include alternative investments (e.g., hedge fund strategies, private investments, or derivatives‑based alternative strategies).

2

The Fund at times may have substantial exposure to a single Style, asset class, sector, country, region, issuer, or currency and companies with similar market capitalizations.

3

A “high-water mark” is a feature associated with performance (incentive) fees generally charged only on new net gains after the investment’s value rises above its previous highest level (after fees). If the investment declines, the value typically must recover above that prior peak before a performance fee may be charged again.

4

A “traditional 60/40 portfolio” generally means a mix of publicly traded stocks and bonds, with roughly 60% stocks and 40% bonds. It does not include alternative investments such as hedge fund strategies, private investments, or derivatives‑based alternative strategies.