Executive Summary

We have a relatively sanguine view on the likelihood of inflation becoming ingrained in the system (much as it pains us to agree with the Fed). However, the dark arts of macroeconomics are notoriously tricky, and we have often talked of the need to build robust (as opposed to optimal) portfolios – effectively, portfolios that can withstand multiple outcomes. As such, it behooves us to consider how to deal with inflation in the context of your portfolio. The first choice you must make is to determine whether you are interested in an inflation hedge (something that closely tracks inflation) or a store of value (something that will preserve purchasing power). For long-term investors, the latter is probably of more interest. A focus on the store of value naturally leads to a search for real assets. Despite conventional wisdom, commodities in general haven’t been a good store of value. The ‘best’ real asset we have found is equities. They make a terrible inflation hedge but over the long term they are the businesses that charge prices and pay wages, so their cash flows should be real if these two elements are roughly matched, and thus they act as a store of value in the longer term. Of course, you can do better than simply buying equities, you can buy cheap equities. This is like being offered inflation insurance at a discount.

Hedging Inflation Risk Today

We have a relatively sanguine outlook on inflation, as discussed in “Part 1: Inflation – Tall Tales and True Causes.” Perhaps you don’t share our view. Or perhaps like us you are always interested in how to build a robust portfolio (one which can survive a lot of different outcomes). Either way it is time to turn our attention to how to protect your portfolio from an inflationary outcome.

As with all ‘tail risk’ insurance you need to ask yourself the three questions that one of us laid out a long time ago.1

1.What are you trying to hedge?

In this case, we need to consider the sources of inflation. Unfortunately inflation seems to follow the Anna Karenina principle. As Tolstoy put it, “Happy families are all alike; every unhappy family is unhappy in its own way”. The ‘good’ news is that the labour market dynamic is truly key for an inflation to take hold so pondering this aspect may make it slightly easier to think about, rather than trying to find the proximate cause.

2. How will you hedge?

We will explore some of the options that you might choose to pursue in the next section of this paper.

3. How much will it cost to hedge?

As always, it is important to remember that insurance is as much a value-based proposition as anything else in investing. So you need to be sure to analyse the cost of the insurance that you are buying.

Before we look at the potential ways you might try to hedge inflation, we need to make a distinction between what we might call hedging and a store of value. We think this is a vital distinction. To us, the term hedge implies a tight correlation with inflation (and therefore takes you into the world of swaps and caps, etc.). The concept of store of value is probably more important to a long-term investor. We think of this as an asset that should outperform inflation but isn’t necessarily closely correlated with inflation (especially in the short term). Equities (assuming fair value for a second) are a real asset and we should expect their underlying cash flows to keep pace with inflation over the long term. As such, they meet the criteria for a store of value. However, due to behavioural issues, sometimes valuations get compressed in inflationary times, so they don’t correlate well with inflation as a hedge. Hence, they are a store of value but not an inflation hedge. Figuring out which of these two dimensions is important to you is vital when it comes to the choices you will make.

Let’s turn to the various instruments that might be thought to act as either a hedge or a store of value when it comes to inflation.

Treasury Inflation-Protected Securities

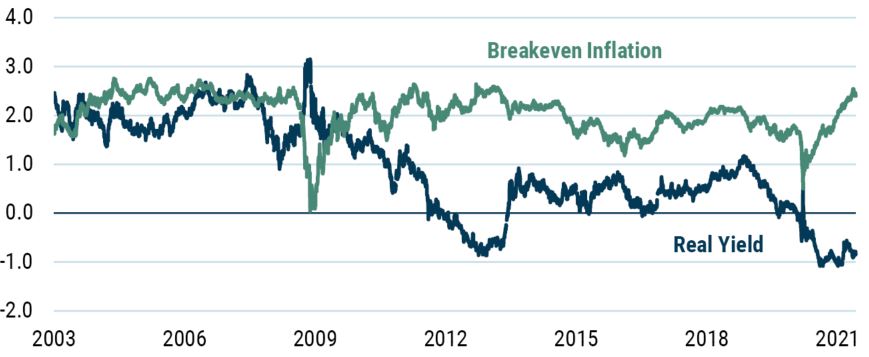

The single most obvious inflation protection is, of course, Treasury Inflation-Protected Securities (TIPS). These are truly indexed to the CPI and have the full faith of the US government behind them. The price you are paying is very clear: right now you are paying around 1% for the privilege of not having to worry about inflation. Obviously, one could also view the inflation breakeven (aka the market’s view of the likely rate of inflation). Currently this market is suggesting inflation of around 2.4% p.a. over the next decade as shown in Exhibit 1.

EXHIBIT 1: US 10-YEAR REAL YIELDS AND 10-YEAR BREAKEVEN INFLATION

As of 6/4/2021 | Source: Federal Reserve

Inflation Caps

An instrument closely related to the above is an inflation cap. These derivative instruments pay out if inflation is higher than the chosen level. For instance, Exhibit 2 shows the price of a 10y 2% inflation cap. Once again, there is no doubt at all that these instruments will hedge inflation, but they do have greater counterparty risk than TIPS.

EXHIBIT 2: PRICE OF A 10-YEAR 2% INFLATION CAP

Source: Bloomberg

Long-standing readers will know we greatly value the reverse-engineered approach, where we ask what we need to believe in order for an asset’s pricing to make sense. In the world of inflation caps and floors, this translates into a probability of inflation exceeding a certain threshold level over the lifetime of the cap. The good folks at the Minneapolis Fed map these inflation cap prices into an easier to understand probability (see Exhibit 3). They don’t go as far out as 10 years, but at the 5-year horizon, the current market price suggests there is a 40% probability of inflation being greater than 3%. So in order to want to hedge with an inflation cap, you would need to believe that there is a higher than 40% chance of 3% p.a. inflation over the next 5 years.

EXHIBIT 3: PROBABILITY OF INFLATION EXCEEDING 3% OVER THE NEXT 5 YEARS

As of 6/30/2021 | Source: Federal Reserve Bank of Minneapolis

Commodities

The conventional wisdom is that commodities are a good inflation hedge/store of value. However, when the data are examined whether one owns exposure to direct spot commodity prices or via futures, it reveals as often that conventional wisdom is not particularly wise. We will examine commodity equities later (wherein we will argue they rely more on their equity nature than their commodity exposure from an inflation protection perspective).

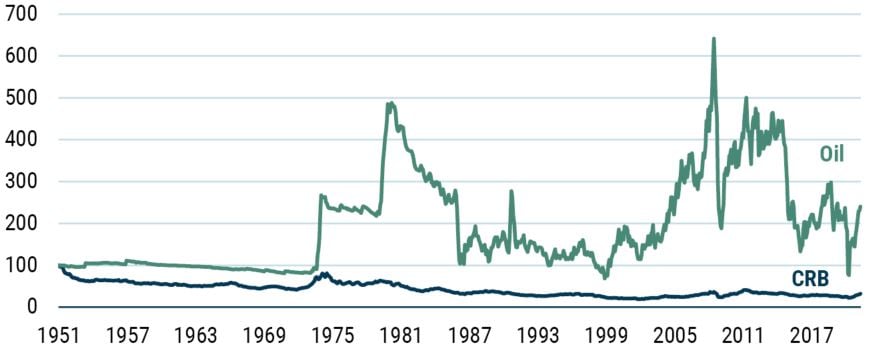

In terms of the store of value perspective, commodities haven’t covered themselves in glory. Exhibit 4 has split commodities into two: oil and the rest (being proxied by the CRB spot commodity price index covering 22 individual commodities). Oil has just about managed to act as a store of value with a real spot return of 1.2% p.a. over this time period (albeit with enormous volatility). Non-oil commodities have not acted as a store of value, with a real spot return of -1.6% p.a. for the sample.

EXHIBIT 4: REAL SPOT COMMODITY PRICES (1951=100)

Data from 1951-2021 | Source: Global Financial Data

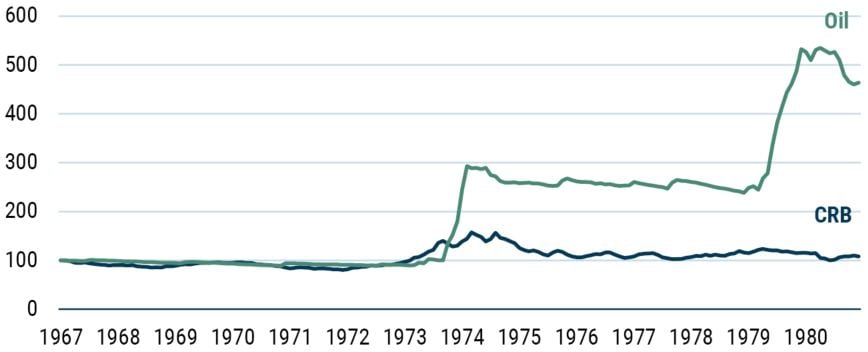

Zooming in on the high inflation era of 1967-80, we see that non-oil commodities just about acted as a store of value, whereas oil did extremely well. The point we’ve made many times before is that oil is the driving reason behind the perception that commodities are a good inflation protection ‘asset’ simply because it was the proximate trigger for the wage price spiral of the 1970s (see Exhibit 5).

EXHIBIT 5: REAL SPOT PRICES (1967=100)

Data from 1967-1980 | Source: Global Financial Data

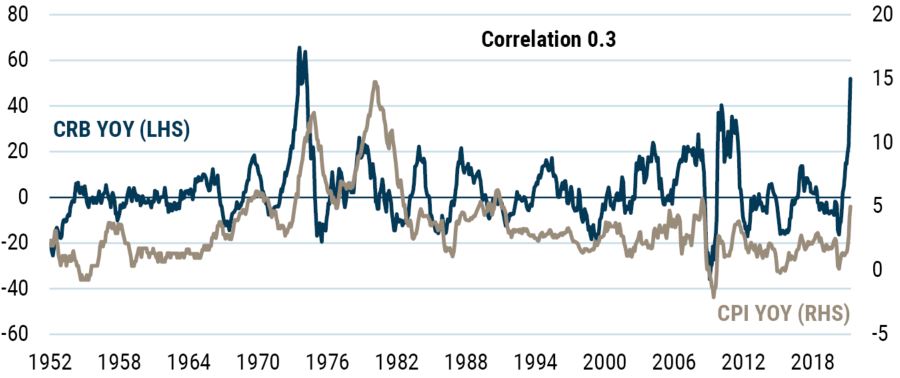

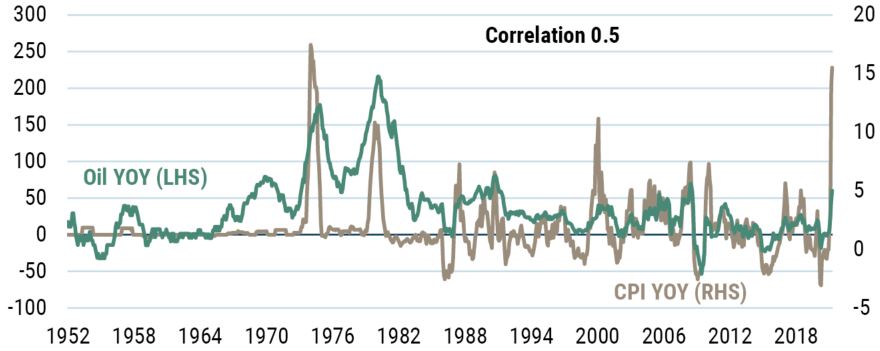

With regard to the shorter-term inflation hedge perspective, once again we see a notable difference between oil and the rest of the commodities complex (for the very obvious reason that oil/gas is a direct component of the CPI). In YOY terms, non-oil commodities show a correlation of 0.3, whilst the oil price shows a correlation of 0.5 with CPI inflation (see Exhibits 6 and 7).

EXHIBIT 6: COMMODITIES VS. CPI YOY – NOT MUCH OF AN INFLATION HEDGE

As of 6/30/2021 | Source: Global Financial Data

EXHIBIT 7: OIL PRICE VS CPI YOY – BETTER BUT NOT GREAT

As of 6/30/2021 | Source: Global Financial Data

Unsurprisingly, oil appears (at least in terms of spot prices) to be the best inflation hedge on the commodity front, due to its inclusion in the CPI itself.

To some extent, the nature of lockdowns means that we should expect to see a short-term demand pressure for commodities once widespread, consistent reopening occurs. However, once again, for this to translate into sustained inflation requires a significant shift in labour market dynamics.

There is, of course, the added issue that investors rarely (if ever) own direct spot commodity price exposure. Positions are generally implemented via futures and, as has been detailed before,2 this is a very different thing from owning spot commodity prices.

The return to a commodity futures position consists of three elements – the spot return, the roll return, and the collateral return. The roll return, of course, depends on the shape of the futures curve. As we have argued before, the greater the participation of ‘investors’ in these markets, the more likely the structure of these markets will be altered. Traditionally (dating back to at least Keynes’ writings in the 1930s) the argument has been that the backwardation should be the norm as producers of commodities are more likely to hedge their price risk than consumers. However, if ‘investors’ or consumers dominate, then an upward sloping futures curve is more likely to be seen (contango). The collateral return simply reflects the fact that the futures take up less cash than a position in the physicals, and thus the surplus cash can be invested into a cash instrument with an obvious yield return.

Exhibit 8 shows the components of the return to the GSCI (a mainly energy-dominated commodity index). As is clearly visible and as was to be expected given the interest rate environment in which we have found ourselves, the collateral return has been markedly lower when one compares the 1970-2000 period to 2000-2021.The spot return has actually been a little higher in the more recent two decades (again thanks to the dominance of energy in this index). However, the roll return has gone from being positive to being massively negative.

EXHIBIT 8: COMMODITY FUTURES RETURN (% P.A. NOMINAL)

As of 6/15/2021 | Source: Goldman Sachs, GMO

All of this adds up to a very different return for investors in the futures relative to the spot. So, in the 1970-2000 period, the spot return to the GSCI was -2% p.a. in real terms, but investors managed to generate an 8% p.a. real return attributable to collateral and roll. In contrast, in the 2000-2021 period, the spot real return was around 2% p.a., but investors in the futures would have realized a negative return of nearly -3.5% p.a.! So once again you can see the importance of understanding the instruments in which you ‘invest’.

Gold

Of course, no discussion of inflation hedges and stores of value can ignore the yellow metal. However, as value investors we have struggled often with gold (which, like the other commodities, doesn’t have a cash flow attached to it and appears to be worth only what someone else is willing to pay).

When it comes to inflation, gold clearly worked as a store of value during the late 1960s/1970s inflation event, generating a 15% real return p.a. between 1967 and 1980. It is far from clear that arguing that gold is a great store of value in inflationary times based on, effectively, a single event is a good idea. Furthermore, without any sense of a fair value it is hard to say what is currently embedded in the gold price (see Exhibit 9). In real terms the gold price is very high (not far off the levels present in 1980). Is this the result of industrial demand, jewelry demand, or embedded inflation fears (which don’t show up in other markets)? We simply have no way of telling. This all makes us nervous because we really don’t have a way of knowing whether we are paying a high or a low price for any insurance properties that gold may offer us.

EXHIBIT 9: REAL GOLD PRICE IN USD

As of 6/30/2021 | Source: Global Financial Data

Bitcoin, et al.

I am sure that some of the fans of cryptocurrencies see them as modern-day versions of gold. We don’t share this enthusiasm. Now, the idea of private currencies isn’t new. Nearly 50 years ago, Friedrich Hayek wrote a short book on the subject entitled “The Denationalization of Money”,3 in which he railed against the dangers posed by a governmental monopoly on money. In his view, competition amongst currencies would stop “the recurring bouts of acute inflation and...also the cure for the more deep-seated disease of the recurring waves of depression and unemployment attributed to ‘capitalism’”. No doubt Hayek would see Bitcoin as a panacea to macro ills.

However, our view is very different. We have a chartist view on the role of money – that is to say we believe money has a worth because we are obliged by governments to pay our taxes in their choice of currency. Put another way, the government will accept its own money back at face value for the settlement of debt (my taxes). Currencies like dollars, pounds, euros, and yen have an issuer that promises to do something in the future – convert them into something else if we are talking about a gold-standard-like regime, or accept them back as payment for taxes if we are talking about a fiat system. The fact that the issuer promises to do something in the future is a liability on the issuer, ergo we can say that the currency is an asset for the holder. Bitcoin and its brethren simply cannot be described as financial assets: they have no attached liability. (Please see the Appendix to this paper for further thoughts about Bitcoin from James Montier.)

Cheap Real Assets

If one is concerned about inflation in the sense of wanting a store of value rather than an inflation hedge, then one obvious thing to do is to seek out sources of cheap ‘real assets’. As noted at the start of this paper, equities are real assets, so cheap equities should be attractive in this setting.

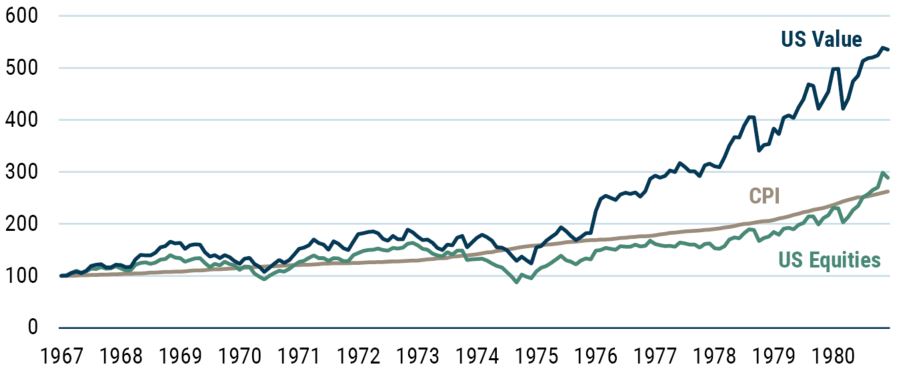

As Exhibit 10 shows, US equities worked as a store of value in the high inflation era despite a massive de-rating, with the overall market dropping from Shiller P/Es of 20.4x to 9x! However, value stocks did much better. Owning cheap real assets seems like a pretty good way to protect yourself against inflation (in terms of store of value).

EXHIBIT 10: EQUITIES DURING THE HIGH INFLATION ERA

Source: Ken French, Global Financial Data, GMO

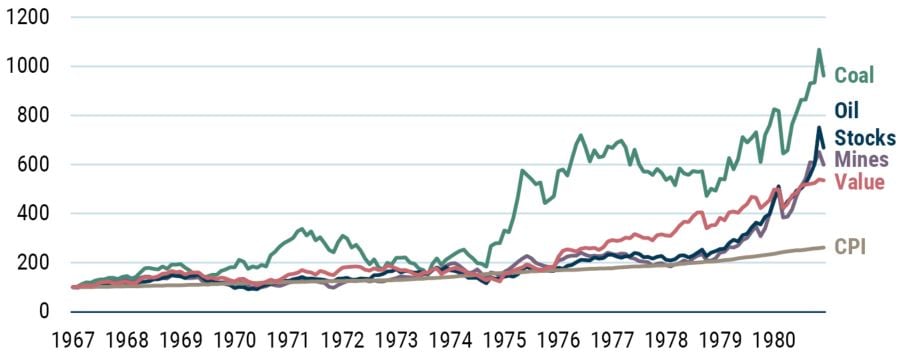

We’ll now turn to commodity equities. We suspect they did much better than the underlying commodities as a store of value because they were cheap – something that today may well be true once again. During the high inflation era there were only three categories of commodity equities – oil, mines, and coal. All of them did well, with coal the clear winner. We’ve included the value group as well in Exhibit 11 for comparison.

EXHIBIT 11: COMMODITY EQUITIES, VALUE EQUITIES, AND INFLATION

Source: Ken French, Global Financial Data, GMO

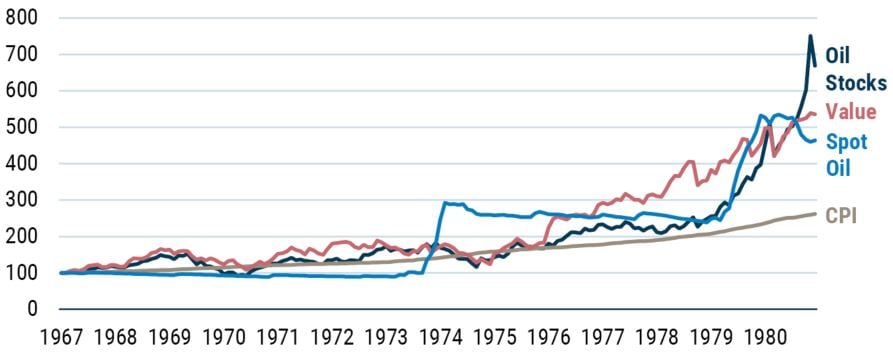

Exhibit 12 shows the performance of spot oil, oil stocks, value stocks, and the CPI. Oil companies performed exceptionally well during the high inflation era, which was not a surprise given the resilience of the oil price and the role it played in inflation creation at that time. But note that value stocks in general also did an exceptionally good job as a store of value (better than spot oil).

EXHIBIT 12: IF YOU ARE LUCKY ENOUGH TO OWN THE PROXIMATE INFLATION TRIGGER

Source: Ken French, Global Financial Data, GMO

Conclusions

We have often talked about the need to build robust portfolios – that is portfolios that can survive multiple outcomes. This desire stems from Elroy Dimson’s excellent definition of risk as “more things can happen than will happen”. So thinking through how to ‘inflation-proof’ a portfolio is always a worthwhile endeavor, even in the absence of a strong inflationary view.

In this regard, an important distinction must be made between inflation hedges and stores of value. The former aim to track the short-term fluctuations in inflation or track inflation very precisely. In this category we have instruments such as inflation-indexed bonds and inflation caps. Of more interest to long-term investors should be assets that act as a store of value (those that maintain or even increase their real purchasing power notwithstanding times of inflation).

Despite conventional wisdom, commodities (outside of oil) are neither a good store of value nor a good inflation hedge. In addition, investors usually gain their commodity exposure through commodity futures, which further muddies the water with the collateral return and roll return components of total return leading investors to experience very different realized outcomes than simple spot commodity prices would suggest.

Gold is often singled out as a great inflation protection. However, from the perspective of a value investor, its lack of fundamental value makes it very hard to determine what is actually in the price, and thus incredibly difficult to determine whether it will, in reality, function as protection. Fans of cryptocurrencies will undoubtedly proclaim that they are the digital version of gold. However, their intrinsic value is effectively zero and, unlike fiat currency, they don’t have the advantage of being a generally accepted payment for taxes. Some may reference their ‘limited’ supply, but whilst this may be true for individual cryptocurrencies, it certainly isn’t true in aggregate (a classic fallacy of composition).

Our best recommendation is to buy true, real assets as a store of value. Foremost amongst these assets is obviously equities. They may make a terrible inflation hedge (as they did during the early 1970s), but over the long term they represent the businesses that charge prices and pay wages, so their cash flows should be real if these two elements are roughly matched. As such, they act as a store of value in the longer term.

Of course, you can do better than simply buying equities. During the last bout of significant inflation, commodity equities were a good store of value (unlike the underlying commodities), and so were value stocks in general. Why? Effectively, you were buying cheap real assets. This is like being offered inflation insurance at a discount. So if you are worried about inflation and looking for a store of value, or you are trying to build a robust portfolio that can survive lots of different outcomes, then buying cheap equities looks like a great place to start.

Appendix

More on Bitcoin

James Montier

As mentioned in the main essay, Bitcoin et al. aren’t financial assets. So, what are they? The closest thing I can come up with is that they are most like commodities. However, unlike most commodities where there is an underlying worth of some description set by their real-world demand and supply, cryptocurrencies are an entirely speculative commodity without any fundamental anchor (akin to works of art without the aesthetic appeal or the limited supply). Occasionally I hear that Bitcoin is digital gold, but gold has value through its demand for jewelry use – its biggest single source of demand – and its industrial use in the electronics industry. Bitcoin and its cousins have neither of these demand sources.

As Keynes warned, “Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation”. We need not be asked to imagine the situation where there is no enterprise at all, but simply a maelstrom of trading. We are in it.

Similarly, Seth Klarman relates, “There is an old story about the market craze in sardine trading when the sardines disappeared from their traditional waters in Monterey, California. The commodity traders bid them up and the price of a can of sardines soared. One day a buyer decided to treat himself to an expensive meal and actually opened a can and started eating. He immediately became ill and told the seller the sardines were no good. The seller said, ‘You don’t understand. These are not eating sardines, they are trading sardines’”.

In part, the love of Bitcoin and its cousins may stem from the general sense of anti-establishmentarianism that seems pervasive today. The rise of social media in driving popular delusions should be clear for all to see. Indeed one of the many dangers of social media is the echo chamber effect it can so easily produce.

A Simple Thought Experiment

There is nothing to stop anyone creating his or her own currency. The problem, as Randy Wray has always opined, has been getting others to accept it. I could easily create ‘Montinotes’. I could print 1 million notes each saying ‘100 Monticoins’, and on each note I could print that the holder of the note has no legal claim against me.

Now, I could try to sell these notes against other currencies, say, the dollar. But what exchange rate should I set? Perhaps 1:1. But why would anyone be willing to spend $100 on a piece of paper that has no intrinsic value and promises nothing? Thankfully, to help us answer that question we have the example of Bitcoin, which is also limited in quantity. (Remember, I printed only one million Montinotes.) By comparison, there is no limit on the quantity of government-created currencies. Thus, Monticoin could trade at a premium to state money.

Going further, I decide not to release all the Montinotes in one go. Instead I am only going to release them slowly over time using the following methodology. I will get together with a group of my colleagues once a week with each of us rolling six dice. If one of us rolls 6 ones, that person will receive 100 Montinotes. Over time I will reduce the number of notes that I issue for a winning roll, so in the second year of the game, for example, I will give out only 50 Montinotes for rolling 6 ones.

Now imagine that for some odd reason this game and the potential for winning Montinotes becomes more and more popular and my friends start to bring their friends to the weekly game. To counteract this increase in players, I raise the hurdle from rolling six ones on six dice, to rolling seven ones on seven dice, and I continue to do this as the number of players grows.

Bear in mind that if I were to move this game into the digital world nothing would fundamentally change. Rather than handing out notes, I would credit them to a virtual account. Non-players could potentially open up accounts to allow them to purchase Monticoin from dice game players. I can even get rid of the real-world game, replacing it with a virtual version.

Thus far there is one big difference between Monticoin and Bitcoin. Monticoin has a central ledger. That is to say that I am keeping a record of all the people who hold Monticoin and the amount they hold, acting as an accountant for the system. Bitcoin uses a distributed ledger. Effectively, this is a decentralized form of ledger that is spread out across different locations and people – everyone within the system can see ‘pages’ of this ledger. There is, of course, nothing to stop me from setting up a distributed ledger for Monticoin, effectively removing myself from the system completely.

The distributed ledger allows everyone to see that Bob received 100 Monticoins from Sally. But because all transactions are recorded, one could also see that Sally received the Monticoins from Harry, who originally won them in the virtual dice-rolling game. A combination of ‘public key’ (encryption for anonymity) and ‘private key’ (think PIN code) is used to allow transfers to occur, just as they do with Bitcoin. All of this obscures my very existence – I have managed to remove myself entirely from the process.

However, nothing has fundamentally changed, Monticoins are still completely worthless and have no claim on any service or utility. They are ‘trading sardines’ at their finest. Yet the collective delusion (think “The Emperor’s New Clothes”) can mean they have a significant price despite having an intrinsic value of zero.

I can think of only two groups that might want to use Bitcoin or one of its cousins. The first are those engaged in essentially illegal activity – the encryption embedded means that users are free from public scrutiny. The second are the deeply paranoid who expect the collapse of the fiat money system. Of course, this group also likes to buy guns and tins of baked beans, and probably prefers hoarding real physical gold (just in case of an EMP attack).

If you are a fan of cryptocurrencies you may still like the idea of limited supply. However, whilst this may be true for any individual crypto, supply isn’t limited across all forms of crypto as my simple thought experiment shows – anyone can create his or her own crypto. Witness the plethora of cryptocurrencies available, with more appearing with steady frequency. (Dogecoin anyone?) The limited supply argument evaporates in aggregate.

To me, cryptocurrencies are the finest example of the inefficiency and insanity of markets. They aren’t even assets. At best they are commodities without the benefit of any real-world use (unlike, say, copper) and boast an intrinsic value of zero. Does that mean that they will crash tomorrow? Of course not. But those involved in this ‘market’ cannot call themselves investors. This is classic trading sardines speculation: a sign of the times!

Download article here.