Overview

Inflation, geopolitical risks, and pending interest rate hikes have brought increased uncertainty and extreme price volatility to global credit markets in 2022. Spreads and yields have increased due to this heightened volatility, creating idiosyncratic opportunities in certain corners of the market. GMO investment professionals Joe Auth, Jon Roiter, Tina Vandersteel and Catherine LeGraw discuss how they are navigating credit dislocations within their areas of expertise.

*This content is intended for accredited investors only.

Within fixed income, we think there is a wonderful hunting ground for alpha opportunities because of breadth and variety…today we find many alpha opportunities that are ranking at top quartile or top decile relative to history.

Catherine LeGraw | Asset Allocation

Key Points

- Areas within the credit spectrum are currently attractive and yielding excellent alpha opportunities. This is an area to consider if you have been under allocated within your fixed income portfolio.

- Within emerging country debt, the spread opportunity between emerging market sub-investment grade sovereigns and investment grade is at one of the highest levels in post-GFC history. The current difference at over 500 bps is 6th percentile for the post-GFC era, and top quartile going back to 1998. In addition, we are finding attractive opportunities within the quasi-sovereign space, where the issuer spread over sovereign has materially widened.

- Within structured products, we see opportunities in fixed rate sectors with high levels of supply. Spreads have widened in commercial mortgage-backed securities, single family rentals, and parts of residential mortgage-backed securities. While duration has ticked up in these corners of the market, their convexity profiles have generally improved, creating upside potential across various pockets of structured credit.

- Within the stressed and distressed credit environment, we are seeing interesting opportunities amongst the mortgage originators, the telecommunications industry, and the emerging markets real estate and gaming sectors. The first quarter of 2022 was one of the worst quarters on record for the high yield asset class, creating an abundance of bonds trading below par that offer the potential for attractive returns and fundamental downside protection.

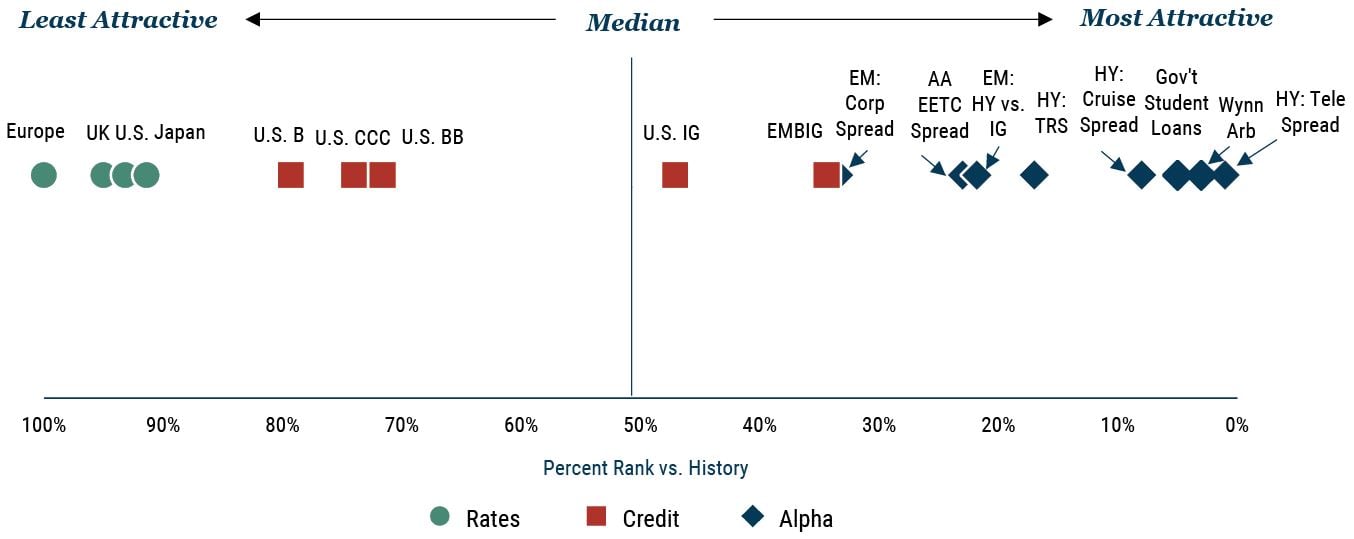

Fixed Income Spectrum of Opportunity

Credit is becoming attractive, and we find excellent alpha potential

PERCENTILE RANK OF FIXED INCOME OPPORTUNITIES ACROSS RATES, CREDIT, AND ALPHA

As of 3/31/2022 | Source: GMO, Global Financial Data, Treasury.gov, JP DataQuery, JP Morgan, Citigroup

Inception of series: 10 year-real yields - U.S.: 1/31/97; UK: 1/31/85; Europe: 6/30/09; Japan: 3/31/04 (real yield is proxied prior to these dates back to 12/31/80 as nominal 10-year yield - prior 10-year CPI). Credit spreads - U.S. BB: 1/31/94; U.S. B: 1/31/94; U.S. CCC: 1/31/94; U.S. IG: 6/30/89; EMGIB: 12/31/1997. EM: HY vs. IG: 1/31/1998; EM Corporate Credit Spread (state-controlled corporates / quasi-sovereigns; country-matched spread): 12/31/14; HY TRS on IBOX (10 day moving average): 3/21/12; Telecom spread over HY Index: 3/12/07; Cruise (proxied by Carinval) spread over HY Index: 12/21/09; American Airlines junior EETC spread over duration matched U.S. Treasuries: 9/9/14; Wynn Macau vs. Wynn Las Vegas spread: 4/11/14; Senior Gov’t Guaranteed Student Loans (10-year tenor) spread over LIBOR: 3/31/10.

Download highlight here.