Executive Summary

Global stocks and bonds are both expensive. U.S. stocks are trading at particularly elevated valuations with the CAPE ratio standing at 35x (vs. a 10-year average of less than 27x) while the Barclays Bloomberg U.S. Aggregate index offered a negative real yield at the end of February. No wonder investors are scouring the earth for attractively priced assets and alpha opportunities. We believe Japan Value and Small Cap Value stocks offer both – a compelling beta opportunity with room for active investors to add value.

We’re excited about Japan Value equities for three key reasons. They offer:

1) attractive valuations;

2) a supportive secular transition of rising profitability and more shareholder-friendly policies; and

3) fertile fishing grounds for alpha seekers.

Japan Value and Small Cap Value Stocks are Cheap

As in other markets, Japanese stocks have risen strongly during the post-Global Financial Crisis cycle. Since the end of 2012, the TOPIX has delivered 12% annualized returns – stronger than ACWI, though trailing the exceptional 15% returns in the U.S. While this has left valuations of Japanese equites stretched relative to historic norms, they do look attractive compared to the U.S. Japanese equities offer higher earnings yields (i.e., cheaper valuations) and stronger expected earnings growth over the next two years.1 Of course, for anyone looking to compound absolute wealth, relative comparisons offer faint praise.

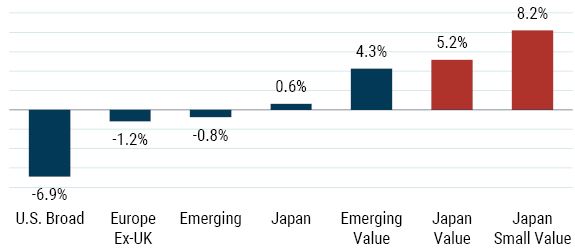

Fortunately, Japanese equities aren’t homogeneous. Value stocks have underperformed dramatically in Japan as they have in other regions for years, leaving their valuations compelling. In addition, while small cap companies have rallied strongly in the U.S. and emerging markets over the last few months, they have not in Japan. Per Exhibit 1, Japan Small Value stocks, which normally trade at a 25% discount to the market, are now sitting at a whopping 46% discount.

EXHibit 1: japan small value trading at an unusually wide discount

As of 1/31/21 | Source: GMO

Price/Scale is based on multiple valuation metrics. Value represents the cheapest half of the market. Small represents the smallest third of the market-by-market capitalization.

This wide discount underpins the appeal of Japan Value equities, but the group’s attractiveness is supported by another key driver: an expectation of improving return on capital levels. Japan has suffered from a combination of low profit levels and inefficient balance sheets for decades, but we are noticing structural and cultural shifts that lead us to believe corporate Japan has “gotten religion” and will improve the return on its capital base toward the levels seen in other developed countries. The combination of expected multiple expansion and rising return on capital leaves Japan Value and Japan Small Value among GMO’s most attractive 7-Year Asset Class Forecasts.

Exhibit 2: japan small value is quite attractive

7-year asset class real return forecasts as of February 28, 2021

Source: GMO. 50/50 Blend of Mean Reversion and Partial Mean Reversion forecasts.

While the tactical, valuation-based opportunity for Japanese Value stocks is strong today, our enthusiasm for the asset class hinges on a view that the improvements we have seen in corporate attitudes and, ultimately, profitability measures are secular in nature, not cyclical.

Equity Market in Transition: Rising Profits and More Shareholder-Friendly Policies

Japan’s path of reforms began in the aftermath of the late 1980s bubble. Following the bursting of a massive asset bubble that saw a rise in bankruptcies or near-death for levered and weak companies, Japanese management teams took steps to bolster their balance sheets and streamline operations. They reduced debt burdens significantly and cut costs more broadly by outsourcing labor, shifting production offshore, consolidating factories, and cutting money-losing products. Of late, labor costs as a percent of revenue have declined as older, more highly paid workers have retired and automation has been deployed.

More recently, policy makers started to institute a comprehensive set of reforms to stimulate growth and make the Japanese economy more competitive by encouraging innovation, reducing regulations, improving governance reforms, and cutting corporate taxes. Former Prime Minister Shinzo Abe accelerated reform efforts that benefitted the interest of equity shareholders.

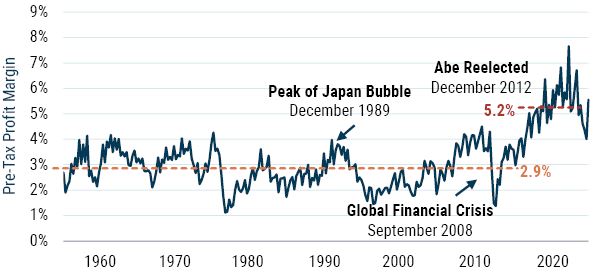

While profits remain cyclical and fell in global stress periods like the Global Financial Crisis and the COVID-19 pandemic, the steps taken have helped improve Japan’s competitive stance and overall profitability. We believe Japanese companies have made durable improvements in their margin structures as illustrated in Exhibit 3, which shows the rise in pre-tax margins2 through time.

Exhibit 3: Japan pre-tax profit margins have improved

As of 12/31/20 | Source: Ministry of Finance

Series commences 3/31/54.

Japan Small Value Stocks Present a Robust Opportunity Set for Alpha Seekers

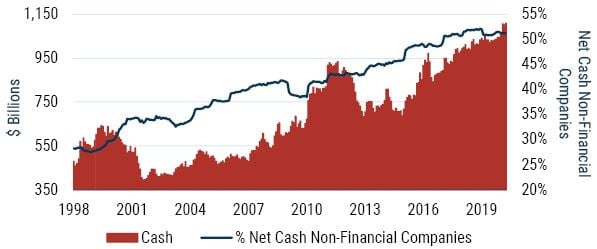

Successful cost cutting, rising profits and free cash flows, and a corporate culture of risk aversion stemming from the bursting of the Japanese bubble led to an ironic side effect: over-capitalized balance sheets. As Exhibit 4 indicates, over 50% of listed non-financial companies are “net cash” today.3 In the U.S., that figure is less than 15%.

Exhibit 4: Excess cash represents low-Hanging fruit and lazy balance sheets waiting to be optimized

Cash Continues to Accumulate

Source: Bloomberg

Carrying large amounts of cash, especially in a negative interest rate environment like today, is troublesome for shareholders. Equity investors expect companies either to reinvest surplus capital in projects that generate returns above the cost of capital or return it to shareholders so they can reallocate to value-creating investments. These “lazy” balance sheets have drawn the attention of Japanese regulators and government, two groups that are trying desperately to spark economic growth to help address the pension burden in a country with a declining population and negative yield on government bonds.

Furthermore, the Japanese equity market is filled with inefficiencies that offer upside opportunities for patient investors. The number of analysts and investors covering the Japanese market has declined following decades of disappointing returns after the bursting of the 1980s Japanese bubble. Cultural and language differences also have diminished foreign investor interest in Japanese equities.

The combination of strong balance sheets, improving profitability, more shareholder-friendly policies, and market inefficiencies has increasingly piqued the interest of investors willing to actively promote minority shareholder interests. The market for corporate control has begun to mature in Japan, shifting from one being hostile to outsiders to an environment more willing to listen to constructive advice. The recent set of cohesive changes in Japan, including corporate governance reforms, the growing influence of proxy voting advisors, and changes in the shareholder structure, is amplifying the voice of minority shareholders. By engaging with management teams, investors can influence investment outcomes and enhance value across an abundant group of attractively priced yet fundamentally sound companies.

In our view, the confluence of cheap valuations, a secular transition in how corporate Japan runs its businesses and considers shareholder interests, and a robust set of asset-rich companies make Japan Value equities compelling not just today, but for years to come.

Download article here.