Executive Summary

Emerging market equity returns have been lackluster in recent years, leading many investors to write off the asset class. Value stocks within emerging markets are particularly cheap, trading at their largest discount since December 2001. While a number of narratives seem to be weighing on the asset class, we believe many of those concerns are overdone. Despite negative headlines and slowing economic growth, emerging market profitability is near its long-term average. While trade wars certainly represent a source of risk for equities across all regions, active management enables us to overweight countries and sectors further from the areas of stress. Today we believe long-horizon investors are being paid to bear the risks embedded in emerging equities, especially emerging value equities, and humbly suggest investors get more comfortable owning the uncomfortable.

Owning emerging market stocks has been a frustrating experience recently. Since the start of 2018, the MSCI Emerging Markets index has fallen 9.5% in USD terms (3.1% local)1 while other markets, the S&P 500 in particular, have rallied. Emerging’s disappointing returns represent the continuation of a long trend of underperformance leading many investors to write off the asset class. We believe that is the wrong move as emerging market stocks – value stocks in particular – represent the best investment opportunity in an otherwise muted landscape. We know from experience that holding an underperforming asset is uncomfortable. At times though, it is warranted. We believe today is one of those times.

What’s To Like About Emerging Market Equities?

While there is plenty to like about broad emerging market stocks, we believe the real opportunity lies within emerging value stocks. They are cheap, offer attractive yields, and are of growing importance due to their size and position among the “global leaders.” Importantly, emerging fundamentals (return on capital and profit metrics) are generally in line with historical levels and do not require overly optimistic assumptions to have a positive expectation of future returns. By using our in-house investment expertise to actively select which countries, sectors, and companies to overweight within the emerging markets, we construct equity portfolios with attractive characteristics. Specifically, the emerging equity portfolio within our flagship Benchmark-Free Allocation Strategy is cheaper and less levered than most equity markets, including the MSCI Emerging Markets Value index.

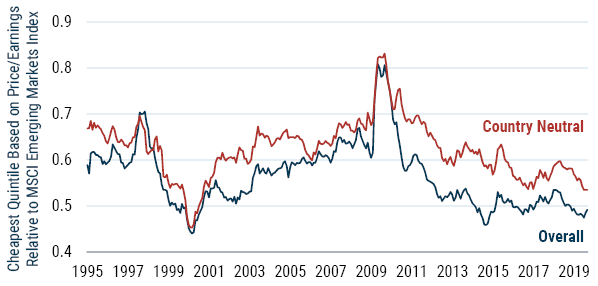

1. Emerging market value stocks are cheap.

Broad emerging stocks look reasonably priced and are attractive relative to other markets. From the end of 2009 through June 2019, the MSCI Emerging CAPE ratio declined from 20x to 15x as compared to U.S. price multiples, which rose from an 18x CAPE to a lofty 29x. When you look further within the emerging universe, as you can see in Exhibit 1, value stocks (in this case defined as the cheapest quintile based on Price/Earnings relative to MSCI Emerging) are particularly cheap, trading at their biggest discount since December 2001. Moreover, we are not expecting extraordinary fundamentals. Our emerging value forecasts assume modestly less than equilibrium levels of growth and income over the next seven years yet result in our highest forecasts due to multiple expansion.

Exhibit 1: Value within Emerging Markets well-Positioned relative to history

As of 9/30/19 | Source: MSCI, S&P/IFCI, GMO

2. Emerging stocks offer higher yields.

At the end of September, the MSCI Emerging and MSCI Emerging Value indexes offered dividend yields of 2.9% and 4.1%, respectively. To provide some context, the S&P yield was a meager 2.0%. On an earnings yield basis, the 10-year normalized earnings yield of 6.1% for MSCI Emerging (as of June) is nearly double that of the S&P’s 3.1% yield. Even in a world in which price multiples stay elevated (no mean reversion), emerging stocks look more attractive.

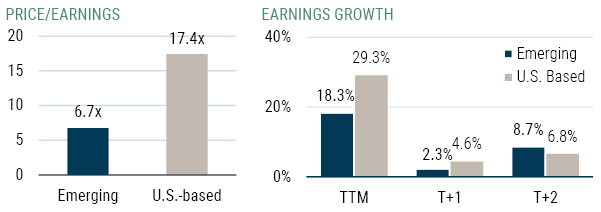

3. Emerging companies are positioned among the “global leaders.”

Emerging countries account for over 40% of both global GDP and the number of publicly traded companies. Eight of the top 20 global companies based on total earnings are domiciled in the emerging markets, trading at significant discounts to the remaining 12 based in the U.S. (see Exhibit 2). While U.S. companies have grown faster recently, analysts expect that growth gap to close in the coming years, with emerging companies eventually surpassing their U.S. counterparts. Although we apply a healthy amount of skepticism to all forward estimates, leading emerging stocks do not deserve to trade so cheaply based on an expected dramatic decline in relative fundamentals.

Exhibit 2: Top 20 Global Company Characteristics

As of 7/30/19 | Source: I/B/E/S, Bloomberg, GMO

Issues Weighing on Emerging Markets

We seek to measure and weigh investment risks relative to the reward on offer. Doing so often requires separating perception from reality. After such a long period of underperformance, the perception about emerging market stocks is dire, with an accompanying number of narratives justifying avoidance.

1. Perception: Emerging markets have weak fundamentals

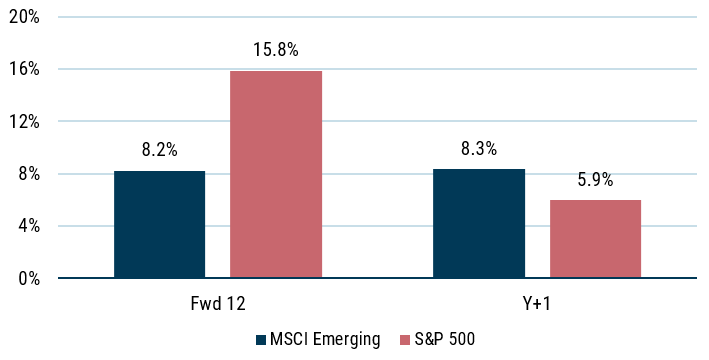

Reality: Despite negative headlines, slowing economic growth, and a modest decline in profitability, fundamentals for emerging markets have not collapsed (see Exhibit 3). Growth and income, as well as return on capital, has been generally in line with historical levels and our forecasted assumptions.2 Looking ahead, analysts are not expecting a dramatic drop in emerging earnings with consensus forecasts for MSCI Emerging actually calling for faster relative growth two years from now.

Exhibit 3: Index EPS Growth

As of 8/28/19 | Source: Bloomberg

2. Perception: Escalation of trade war tensions will crush emerging.

Reality: It is difficult, if not impossible, to predict future policy moves and their impact on the long-run earnings power of individual companies, sectors, and countries. It does appear that tariffs have hit Chinese company EPS harder than in the U.S., a fact relative prices have not ignored. While harder to quantify at this stage, an all-out trade war would impair the global economy and impact all players, including the U.S. Within our emerging portfolios, we view trade wars as a source of risk and monitor our positions in order to ensure that this risk is contained. We believe our current emerging markets portfolio within the Benchmark-Free Allocation Strategy is well-positioned to withstand the pressures of the current trade war. Our overweight positions in Russia and Turkey, which we don’t expect to be materially impacted by trade war concerns, and preference for China-A shares names with higher domestic exposure, could provide some relative defense. In addition, we have opposing stands on the two emerging countries arguably most geared to global trade – Korea and Taiwan. Today, we are significantly underweight Korea and significantly overweight Taiwan.

3. Perception: If U.S. stocks decline, emerging will drop even more.

Reality: If the U.S. market sold off meaningfully, we would expect emerging stocks to fall more under most scenarios, however, three things provide us the fortitude to favor emerging today. First, MSCI Emerging’s current relative valuation discount could help shield losses. After the Internet bubble began to implode, MSCI Emerging offered shelter in 2002 – the still expensive S&P 500 declined 22% for the year while MSCI Emerging fell only 6% due to relatively low starting valuations.

Second, emerging market rebounds can be strong and quick. In 2003 and 2004, MSCI Emerging rallied an impressive 96%, cumulatively doubling the S&P 500’s 43% gain due to reasonable valuations and enthusiasm stoked by China joining the World Trade Organization. Investors who held emerging stocks from the end of 1999 through 2004 ended with nearly 40% more wealth than the broad U.S. market (which fell 12% in nominal terms).

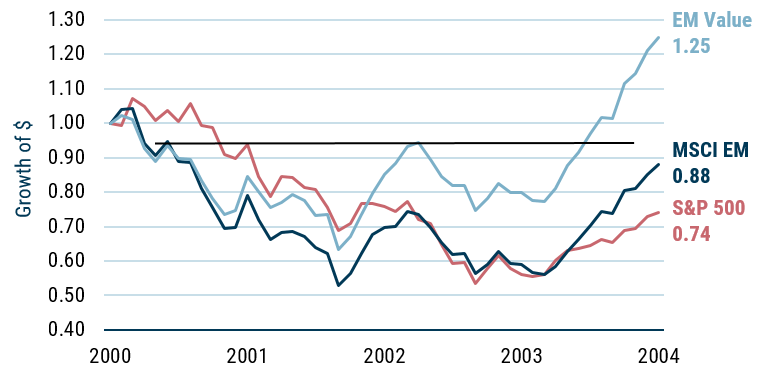

Third, even when the broad emerging market index experiences declines, the value universe within can provide stability, especially when it is priced cheaply. While emerging value stocks3 fell during the depths of the bursting of the Internet bubble, they delivered positive cumulative returns of 25% over the 4 years ended January 2004 while the S&P 500 and MSCI Emerging indexes remained 26% and 12% below water (see Exhibit 4). Value stocks were priced to outperform coming into that cycle much as they are today. On a price to economic book4 measure, the S&P 500, MSCI Emerging, and emerging value stocks were trading at 3.8x, 2.1x, and 1.3x, respectively, at the end of January 2000. Today, those figures are 3.0x, 1.6x, and 1.1x, respectively. A similar pattern of emerging value outperformance played out in the 1995-98 market sell-off.

Exhibit 4: Internet Bubble Index Performance

As of 1/31/04

4. Perception: The USD has been strong and will continue to rise.

Reality: Emerging currencies look cheap on purchase-power-parity valuation metrics and still offer attractive carry. We recognize the strong current demand for USD funding but believe the multi-year headwind pushing down emerging currencies will likely turn to a tailwind in the years ahead.

Getting Comfortable Owning the Uncomfortable

Fatigue may be the most common complaint against owning emerging equities these days. Emerging has underperformed for a long period and it is hard to see a catalyst for a turn. Predicting the short-run, though, is quite challenging. After all, while we and many others pointed out the dangers of absurd valuations during the TMT bubble, the catalyst that led to its unwind is still not apparent decades later. We focus on valuation, which has been a wonderful predictor of future returns. At GMO, we employ a long-horizon approach, sizing our emerging equity exposure so it is meaningful given its absolute and relative attractiveness, and tilting it to emerging value given the additional attractiveness we find here in our country, sector, and security selection.

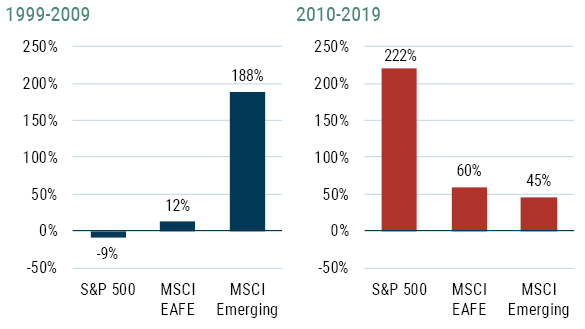

Owning a cheap asset class rarely feels good. Human nature leads investors to extrapolate current conditions and chase recently outperforming assets, both of which lead to stretched valuations and changing investor enthusiasm. After nearly a decade of the relative underperformance of emerging stocks, many seem to have forgotten the distaste investors harbored for U.S. stocks just 10 years prior (see Exhibit 5).

Exhibit 5: Enthusiasm shifts…and will likely shift again

As of 6/30/19 | Source: GMO

A decade ago, emerging equities had just delivered superlative performance as China’s inclusion in the World Trade Organization and seemingly insatiable demand for resources stoked investor enthusiasm. Investors at the same time worried the U.S. was losing its manufacturing base and was a slower growing economy. Post the Global Financial Crisis, investor enthusiasm has clearly flipped.

Today we believe long-horizon investors are being paid to bear the risks embedded in emerging equities, especially emerging value equities, and humbly suggest investors get more comfortable owning the uncomfortable.

Download article here.