The world seems an increasingly uncomfortable place for traditional stock and bond investments. Despite dramatic repricing (with the MSCI ACWI down 26% and the Bloomberg U.S. Aggregate Index down 15% YTD through 9/30/22), there is little optimism that the carnage is over.

We have long said that valuations are stretched and that investors should be cautious when it comes to their level of exposure to market beta. One of the reasons that we remain excited about the long Value vs. short Growth trade is the fact that it is broadly equity beta neutral – a very desirable characteristic in this time of heightened uncertainty. It has been an oasis of positive performance so far in 2022. 1 The GMO Equity Dislocation Strategy is our active, risk-controlled approach to exploiting the Value-Growth opportunity. The Strategy is long the cheapest Value stocks and short the most expensive Growth stocks, and it is approximately beta neutral.

To hypothesize on the future success of this trade, it is interesting to consider the potential drivers of relative performance.

Interest rates: No clear link to Value relative performance

A narrative of low rates justifying high valuations for supposedly longer-duration Growth stocks seems to have been a force behind Growth stocks hitting bubble levels. However, we do not believe there is an underlying fundamental connection 2 and historically there was little correlation (see chart below). If the Market latches onto a narrative, investor sentiment and behavior can render it self-fulfilling in the short term; witness the recent dramatic rise in the correlation between yield changes and Value performance. While higher inflation (and rates) began the unwind of the Value-Growth gap, our expectations for the future of the Value trade remain grounded in fundamentals and therefore are not predicated on any particular path for rates.

Value vs. Growth: Weak and Unstable Relationship to Rate Changes

Correlation between yield change and Value vs. Growth rolling 36 months

As of 9/30/2022 | Source: MSCI, Federal Reserve

Correlation is between the monthly yield change on the constant maturity 10-year U.S. Treasury and the monthly return of MSCI U.S. Value less MSCI U.S. Growth.MSCI data may not be reproduced or used for any other purpose. MSCI provides no warranties, has not prepared or approved this report, and has no liability hereunder. Please visit https://www.gmo.com/americas/benchmark-disclaimers/ to review the complete benchmark disclaimer notice.

Recession: No clear link to Value relative performance

More recently, the Market may have retrained its sights away from interest rate rises, and the crosshairs are now highlighting the possibility of a recession. Against this backdrop, Growth has actually outperformed Value by a couple of points for the third quarter. There is, of course, some logic in this as many of the lower-quality and cyclical Value stocks may struggle if we move into a recession. We believe that accounting for the quality of the company when determining whether the stock is cheap or expensive helps mitigate this risk. 3 Further, it is not obvious that Value would underperform in a recession; in fact, historically there’s been a slight tendency for Value to outperform in economic downturns. 4

Valuation remains favorable

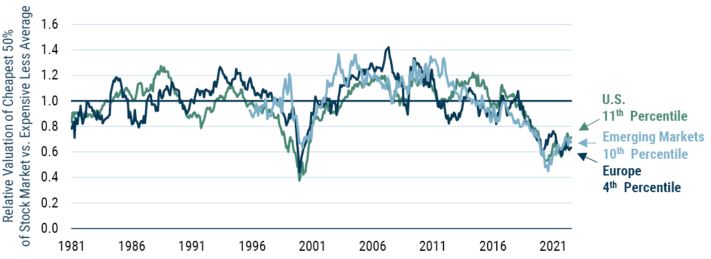

Crucially, what both of those arguments are failing to take into consideration is valuation. We believe that Value will outperform Growth purely and simply because it is priced to do so. While Value has repriced meaningfully relative to Growth, this remains an extreme valuation dislocation that we believe is likely to continue to unwind. Value has retraced roughly halfway back to normal, so considerable reversion remains to return to the historic median relative valuation (1.0 on the chart below).

Value Remains Quite Cheap Globally

As of 9/30/2022 | Source: GMO

Composite Valuation Measure is composed of price/sales, prices/gross profit, price/book, and price/economic book.

Ultimately, valuation is the anchor for investments and there is an inexorable pull back to fair value. Growth will underperform because it is priced for unrealistic expectations and will falter as companies fail to live up to those expectations. Sentiment will shift, and the path to continued Value outperformance is unlikely to be a straight line. We have seen this before 5 and are reasonably sanguine about it, not least because the emphasis on quality and the risk-controlled approach to portfolio construction in the Equity Dislocation Strategy may help to smooth out any bumps in the road ahead.

Download article here.

MSCI ACWI Value outperformed MSCI ACWI Growth by 13.1% from 12/31/21-9/30/22. Preliminary performance for GMO’S Equity Dislocation Strategy was up 13.7% gross (11.9% net) over the same period. Performance data quoted represents past performance and is not predictive of future performance. Net returns are presented after the deduction of a model advisory fee and incentive fee if applicable. These returns include transaction costs, commissions and withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. A Global Investment Performance Standards (GIPS®) Composite Report is included in the Important Information section at the back of this presentation. GIPS® is a registered trademark owned by CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Actual fees are disclosed in Part 2 of GMO's Form ADV and are also available in each strategy's Composite Report. Final performance numbers are generally available on GMO’s website five to ten business days after month end. Investors should not rely on preliminary numbers to make investment decisions.

See “The Duration of Value and Growth: Much Closer to Each Other Than You’d Guess,” by Ben Inker (March 2021).

Despite emphasizing very cheap stocks, the GMO Equity Dislocation Strategy’s long book has a historic one-year median Return on Equity (ROE) of 14.8%, which, although about 20% less than the MSCI ACWI equivalent of 18.5%, is far superior to the short book – which is not only egregiously expensive, but also has a paltry historic one-year median ROE of just 8.6% as of 8/31/22.

See GMO’s 2Q 2021 Quarterly Letter, “Dispelling Myths in the Value vs. Growth Debate,” by Ben Inker (August 2021).

See “Value Vs. Growth Reversals: Never a Straight Line,” by the Asset Allocation team (July 2021).

Disclaimer: The views expressed are the views of the Asset Allocation team through the period ending October 2022, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2022 by GMO LLC. All rights reserved.

MSCI ACWI Value outperformed MSCI ACWI Growth by 13.1% from 12/31/21-9/30/22. Preliminary performance for GMO’S Equity Dislocation Strategy was up 13.7% gross (11.9% net) over the same period. Performance data quoted represents past performance and is not predictive of future performance. Net returns are presented after the deduction of a model advisory fee and incentive fee if applicable. These returns include transaction costs, commissions and withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. A Global Investment Performance Standards (GIPS®) Composite Report is included in the Important Information section at the back of this presentation. GIPS® is a registered trademark owned by CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Actual fees are disclosed in Part 2 of GMO's Form ADV and are also available in each strategy's Composite Report. Final performance numbers are generally available on GMO’s website five to ten business days after month end. Investors should not rely on preliminary numbers to make investment decisions.

See “The Duration of Value and Growth: Much Closer to Each Other Than You’d Guess,” by Ben Inker (March 2021).

Despite emphasizing very cheap stocks, the GMO Equity Dislocation Strategy’s long book has a historic one-year median Return on Equity (ROE) of 14.8%, which, although about 20% less than the MSCI ACWI equivalent of 18.5%, is far superior to the short book – which is not only egregiously expensive, but also has a paltry historic one-year median ROE of just 8.6% as of 8/31/22.

See GMO’s 2Q 2021 Quarterly Letter, “Dispelling Myths in the Value vs. Growth Debate,” by Ben Inker (August 2021).

See “Value Vs. Growth Reversals: Never a Straight Line,” by the Asset Allocation team (July 2021).