Humans are hardwired to enjoy gambling. It provides a dopamine hit by triggering the brain's reward system, a response strongly linked to the unpredictability of reward, not just winning. Despite everyone knowing that “the house always wins,” the commercial casino gaming revenue for the state of Nevada grew to a record $15.8 billion in 2025. Or, closer to GMO’s headquarters in Massachusetts, lottery players spend over $1,000 per person annually—more than triple the national average of just over $300 per person across 45 participating states.

Growth investing has a return distribution much more akin to gambling than value investing, and most would agree that being a growth investor is a lot more “fun” than being a value investor. Everybody loves the idea of investing in the next Amazon or Nvidia. But we would argue that a strong reason to consider value investing is that, while it is potentially less exciting, your expected return is higher.

Stack the odds in your favor

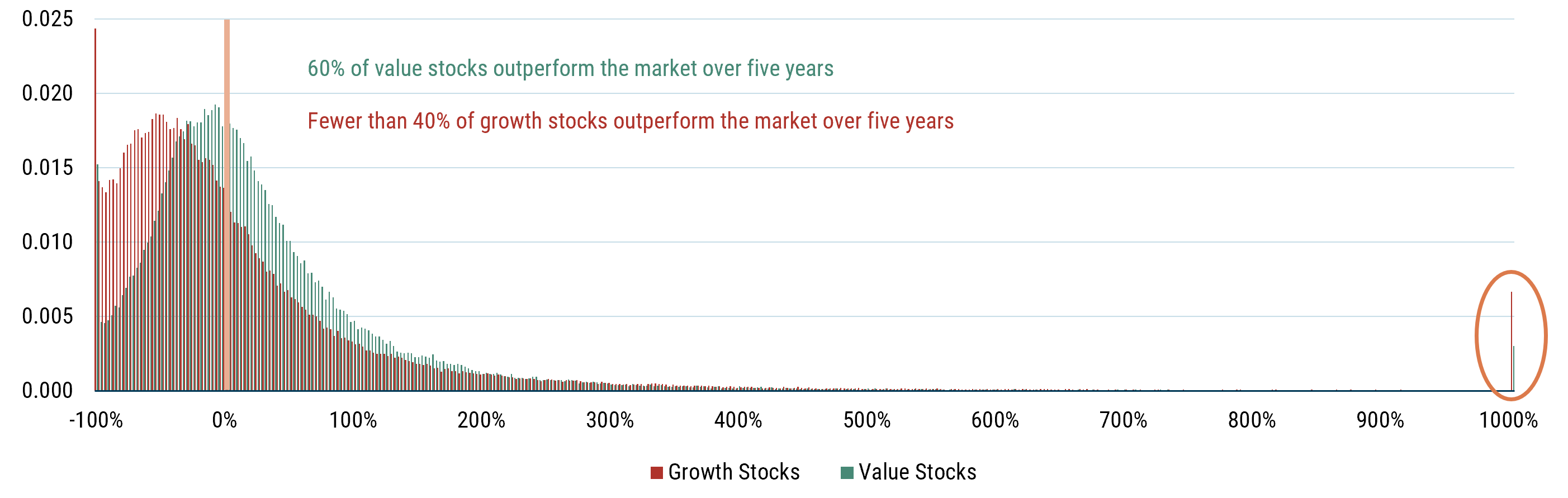

To begin with, the odds are skewed in your favor: over five-year horizons, 60% of value stocks (Exhibit 1, green bars) outperform the market. At the extremes, a small number of value stocks do go bankrupt (Exhibit 1, far-left green bar), while a few deliver truly extraordinary returns (Exhibit 1, far-right green bars, which show stocks that increased by at least 10x).

EXHIBIT 1: U.S. STOCKS ARE LOTTERY-LIKE

Average 5-year relative return distribution of U.S. value and U.S. growth stocks

As of 9/30/2025 | Source: Bloomberg, Compustat, Worldscope, MSCI, GMO

Growth stocks (Exhibit 1, red bars) offer a very different return distribution, with perhaps the most noticeable difference being that over twice as many growth stocks go on to become 10-baggers. But chasing these success stories has an unpleasant downside–one that is often ignored as inconvenient stocks simply vanish from growth portfolios and are never mentioned again. The proportion of growth stocks that go bankrupt is over 50% higher than that of value stocks (Exhibit 1, far-left red bar), while fewer than 40% of growth stocks have outperformed the market over five-year time frames.

What about valuation?

Given that the price paid for any asset is a crucial determinant of potential return, at GMO we believe that all investors should be valuation-aware investors, not just dyed-in-the-wool growth or value investors. Although value stocks have, on average, delivered better returns than growth stocks, starting valuations could potentially skew the balance toward growth stocks from time to time. For just over a decade, starting in 2005, narrow valuation spreads between value and growth stocks suggested a poor environment for value in the U.S. 1 Today, however, valuation spreads are extremely wide. With all the buzz around the transformative potential of artificial intelligence, investors’ willingness to pay up to chase the lottery-like payoff of growth stocks is at historic extremes, making it a particularly compelling time to favor value stocks.

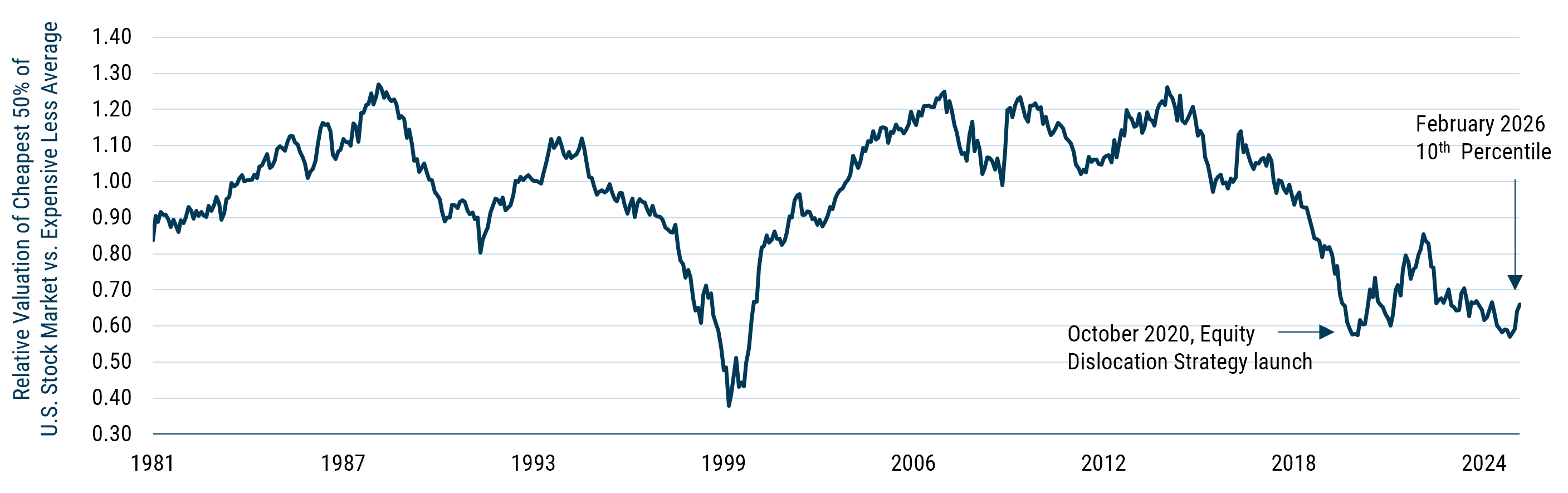

Exhibit 2 shows the relative valuation for U.S. value stocks compared to U.S. growth stocks, normalized so that 1.0 represents the median. Today, value stocks are trading at an approximate 35% discount to their typical relative valuation, a 10th percentile observation vs. history. Value needs to beat growth by almost 55% just to return to historically normal relative valuations.

EXHIBIT 2: VALUE IS EXTREMELY CHEAP

As of 2/28/2026 | Source: GMO

Stock valuations are calculated on a blend of Price/Sales, Price/Gross Profit, and Price/Economic Book.

Even if this abnormally wide valuation spread does not narrow immediately, we believe value can still outperform due to what we call the rebalancing effect. Value benefits as some growth companies disappoint and become cheaper, entering the value index. Value also benefits as some value companies surprise on the upside and get repriced into the growth index. This effect is particularly pronounced when valuation spreads are wide since the valuation change associated with a move from value to growth or growth to value is large. (In the context of an active strategy, such as our long value/short growth Equity Dislocation Strategy, this rebalancing effect is demonstrated as strong security selection. From the end of 2022 through the end of February 2026, security selection has helped the Equity Dislocation Strategy deliver a net return of 6.3% per annum, despite MSCI ACWI Growth beating MSCI ACWI Value by some 8% per annum over the same period.)

How can you best monetize this dislocation?

- Equity Dislocation seeks to directly profit by going long the cheapest value stocks and short the most expensive growth stocks in a market-neutral portfolio.

- Dial into deep value through long-only equity portfolios, like U.S. and International Opportunistic Value, which target the cheapest cohort of stocks.

For more, see Ben Inker’s 2005 piece, “The Trouble with Value,” available from your GMO representative.

Disclaimer: The views expressed are the views of the Asset Allocation team through March 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Past performance is no guarantee of future results.

Copyright © 2026 by GMO LLC. All rights reserved.

For more, see Ben Inker’s 2005 piece, “The Trouble with Value,” available from your GMO representative.