- Investors have been chronically underweight Japan for the past three decades, and rightly so given Japan’s weaker relative fundamentals and underwhelming commitment to corporate reform through much of the 1990s and 2000s.

- But conditions on the ground have changed meaningfully. Improving fundamentals and governance reforms are increasingly evident to investors speaking directly with companies and policymakers in Japan, as our Usonian Japan Equity team does. EPS growth has been relatively strong in Japan for years, distributions of excess capital have increased, and policymakers continue to push for more competitive and capital-efficient companies.

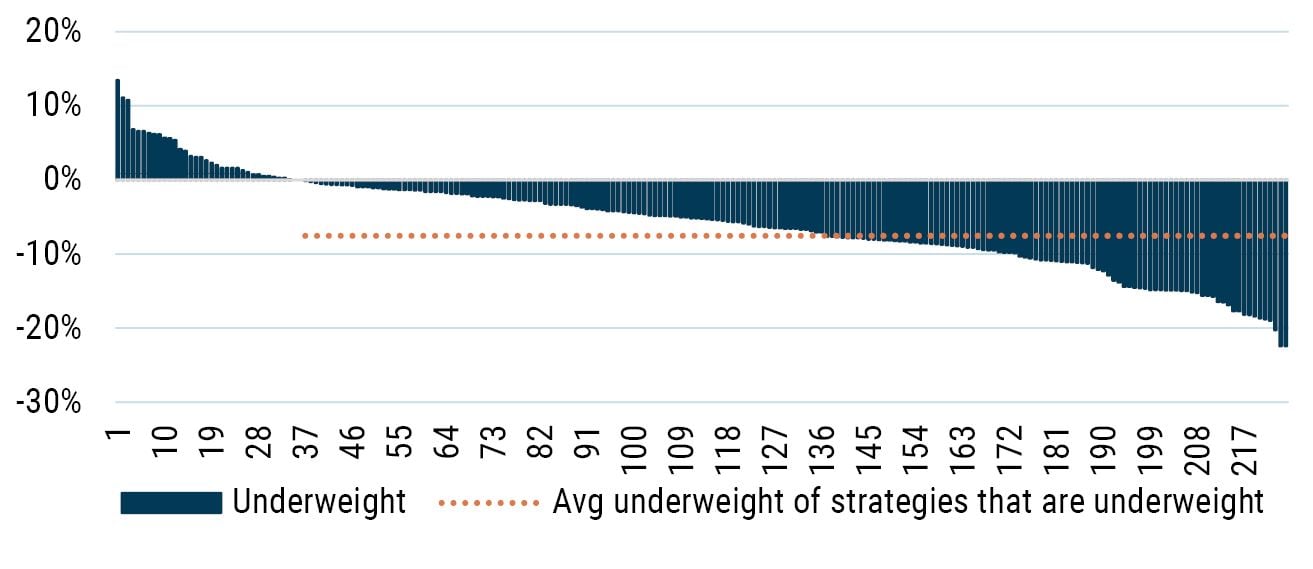

- Nonetheless, most international equity strategies remain materially underweight Japanese equities. Of 225 actively managed strategies in the eVestment database that list the MSCI EAFE index as their preferred benchmark, 1 84% are underweight Japan by an average of 7.5% as the chart below indicates.

MSCI EAFE Active Manager Over/Underweights to Japan (by strategy)

As of 6/30/2023 | Source: eVestment

- In our view, the reasons so many active managers are underweight Japan stem from firm structural issues and biases, rather than fundamental analysis:

- Following the burst of Japan’s asset bubble, both the sell side and buy side significantly cut resources in Japan. To cover Japan, investment managers based in global financial centers, like New York and London, must endure extremely inconvenient logistical challenges (time zone differences and travel times), cultural challenges (language and otherwise), and idiosyncratic structural quirks of doing fundamental research and investing in Japanese equities. Most opted to allocate research resources to other markets. To the degree that managers have Japan exposure, they tend to do so through ADRs and “gaijin 2 favorites.” Very few are pounding the pavement to speak with management of small-to-mid cap listed Japanese companies, which is where we find most of the exciting opportunity.

- We have seen renewed interest in Japanese equities this year which has led to foreign inflows, but most of it has been indiscriminate purchases of futures and ETFs. Many investors we speak with are underweight Japan but looking to close the gap. Those relying on their developed market equity managers to do so may be disappointed though, because most do not have the structure capable of navigating Japan’s market nuances.

- Perhaps this underweight Japan bias among MSCI EAFE managers will dissipate. Any increase in institutional flows would be a welcome tailwind as our research suggests trailing inflows portend good things for near-term sentiment and subsequent returns. But investors may miss an attractive opportunity as they wait.

- At GMO, we’ve already been positioned for the good news we expected. The GMO International Equity Strategy is among the most overweight to Japan in the category with a 3.4% overweight and GMO’s more flexible Global Equity Allocation and International Equity Allocation Strategies have similar or larger overweights of 6.5% and 4.2% relative to their respective benchmarks. 3

Download article here.

1

Universe includes All Cap Core, Growth and Value and Large Cap Core, Growth and Value active strategies within the eVestment All EAFE Equity universe.

2

Gaijin refers to foreigners or outsiders, typically of non-East Asian ethnicities.

3

As of 8/31/23.

Disclaimer: The above information is based on a representative account within the strategy selected because it has the fewest restrictions and best represents the implementation of the Strategy.

The views expressed are the views of Drew Edwards and Rick Friedman through the period ending October 2, 2023, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2023 by GMO LLC. All rights reserved.

1

Universe includes All Cap Core, Growth and Value and Large Cap Core, Growth and Value active strategies within the eVestment All EAFE Equity universe.

2

Gaijin refers to foreigners or outsiders, typically of non-East Asian ethnicities.

3