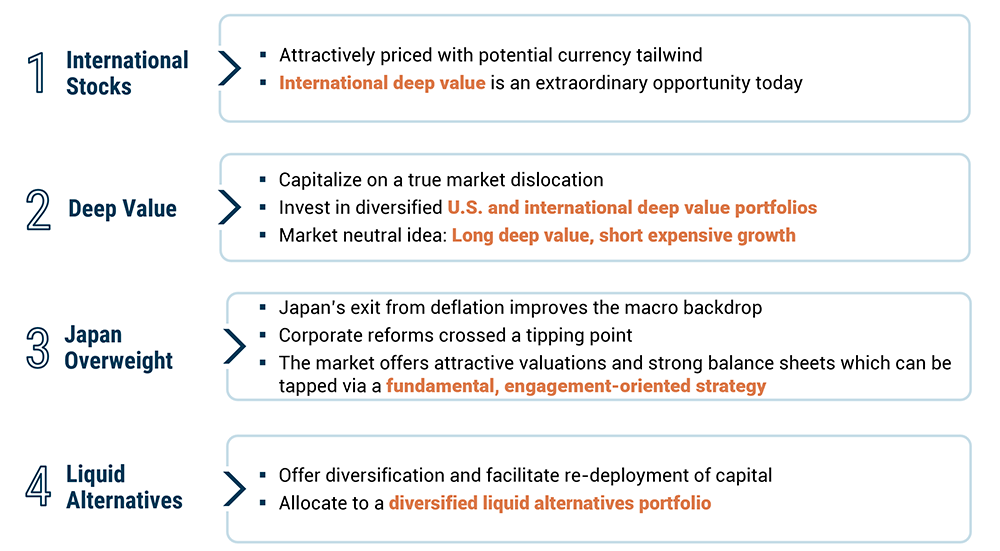

Thanks to strong gains in markets over recent years, with many indices at or near record highs, the 60/40 default portfolio has quietly morphed into a bundle of expensive U.S. growth equities and credit exposures offering narrow spreads over Treasuries.

In our view, such a portfolio is likely to disappoint investors by delivering low single-digit real returns. Yet, we are enthusiastic about the investment landscape.

An abundance of assets ranging from fairly valued to downright cheap underpins this outlook from an absolute return standpoint, while appealing valuation spreads within asset classes present us with the best relative asset allocation opportunity we’ve seen in 35 years.

Within GMO’s Benchmark-Free Allocation Strategy, a valuation-sensitive strategy that is willing and able to be dynamic, we’ve identified and dialed into four current market dynamics to build portfolios with some of the highest forecasted relative and absolute returns we’ve ever seen.

GMO Asset Allocation “Big Bets”

- Non-U.S. equities are cheap relative to the U.S., and cheap currencies add a tailwind.

U.S. equities have delivered solid fundamental performance, in line with our long-term assumptions, but have also seen their multiples rise significantly in recent years.

Across many valuation metrics, including CAPE ratios, the U.S. is trading at or near its largest premium ever relative to the rest of the world.

For those who argue a CAPE ratio is somehow missing the fact that U.S. equities are massively better fundamentally than they were a decade ago, valuations on a price-to-forward earnings basis (which embeds forward-looking growth on top of today’s high earnings) look every bit as stretched, with the U.S. trading at an over 50% premium to its long-run average.

Markets in the rest of the world, however, are trading at or below their long-run averages, creating a huge gap in relative valuations to the U.S. Not only do non-U.S. stocks benefit from attractive valuations, but they also stand to profit handsomely from cheap currencies.

Equity investors can capture the benefit of cheap currencies in two ways: either the currencies can appreciate back toward fair value, or the companies can exploit the competitive advantage of lower relative costs to boost earnings growth. Japan small value equities are particularly compelling today, driven by their absolute and relative cheapness, the underlying secular changes in corporate governance and profitability, and a record cheap currency. - Deep value is extremely dislocated.

The cheapest 20% of markets, which we refer to as deep value, are severely dislocated, trading at 3rd and 7th percentile discounts compared to history in the U.S. and developed ex-U.S. markets, respectively.

Value, especially its cheapest cohort, offers outperformance through two channels: as the discount the group trades at normalizes, and as cheaper stocks benefit from what we call rebalancing.

Rebalancing stems from the fact that value is not a static strategy. Cheap companies as a group don’t grow as fast as the average company, but some of them wind up positively surprising investors. As the better-than-expected results and outlook cause investors to look more favorably at those companies, their valuations rise even if the rest of the value group continues trading at a large discount. Such stocks wind up leaving the value universe, but they perform very well on their way out.

At the same time, other companies that were expensive and in the growth universe disappoint investors and see their valuations fall. Such stocks, originally in the growth universe, see quite poor returns but give a fresh source of newly cheap companies upon entering the value universe, replacing those value companies whose positive surprises led to upward revaluations.

The rotation of cheap companies entering the value group as the relatively more expensive stocks exit provides a meaningful tailwind to relative returns, even in an environment where the overall spread between growth and value stock valuations remains the same. Importantly, the wider the value spread (like we see today), the more impactful rebalancing tends to be.

We are leaning heavily into this compelling opportunity across our portfolios through our long-only U.S. Opportunistic Value and International Opportunistic Value strategies.

Thanks to the robust opportunity set for deep value, a holistic view of value, and thoughtful portfolio construction constraints, both U.S. and International Opportunistic Value trade significantly cheaper than broad value benchmarks but are of higher quality when viewed through the lens of debt-to-equity and ROE metrics. - Japan should benefit from structural change and attractive valuations.

Japanese equities represent a compelling opportunity driven by a confluence of structural, macroeconomic, and valuation-based factors.

After decades of deflation, Japan is undergoing a profound transformation marked by sustainable inflation and a shift in corporate behavior toward shareholder-friendly practices.

Corporate reforms – such as increased buybacks, unwinding of cross-shareholdings, and a more active market for corporate control – are accelerating, while policy initiatives like the Tokyo Stock Exchange’s 1x PBR campaign and Kishida’s “Asset Management Nation” are reshaping governance and capital allocation norms.

Despite these improvements, global investors remain significantly underweight Japan, creating a compelling contrarian opportunity. Benchmark-Free is positioned to capitalize on this dislocation, particularly in small value stocks, which trade at historically wide discounts and are poised to benefit from both structural tailwinds and an undervalued yen.

Given the abundance of publicly traded small and mid-size companies with overcapitalized balance sheets, the Japan market offers an attractive opportunity to generate alpha through a fundamental, engagement-oriented investment approach. - The historically wide spread between value and growth sets up a compelling long/short opportunity.

Of course, deep value is not the only group that is dislocated. Growth broadly is trading expensively relative to its history. In fact, the most richly priced 20% of markets (e.g., extreme growth) are trading at 92nd and 93rd percentile premiums compared to history in the U.S. and developed ex-U.S. markets, respectively.

The spread between the extreme growth and deep value cohorts is excessively wide today, creating an opportunity for a long/short strategy to benefit should relative valuations narrow.

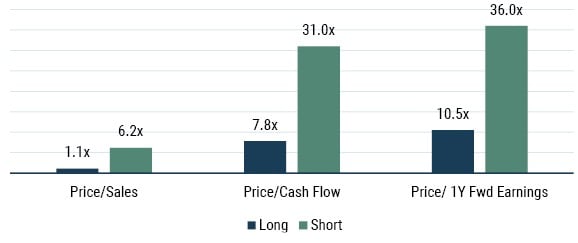

GMO’s Equity Dislocation Strategy, which is 100% long deep value and 100% short extreme growth stocks (and the largest single exposure within Benchmark-Free), seeks to benefit from this aberration.

As the exhibit below indicates, there is a huge gap in the characteristics between our longs and our shorts. Our long portfolio is trading at somewhere between one-third and one-fifth the valuation of the short portfolio.

Exhibit: Equity Dislocation Strategy

Leveraging the wide gap between value and growth to deliver diversifying returns

As of 6/30/2025 | Source: GMO

Portfolio characteristics are subject to change. The above information is based on a representative account in the strategy selected because it has the fewest restrictions and best represents the implementation of the strategy.

As in the case of value, spread narrowing isn’t the only way a long/short strategy can win. Such a strategy benefits from both sides of the rebalancing process described above by being long value stocks that leave the universe with higher valuations than they entered with and shorting growth stocks that disappoint.

If growth stocks are trading at huge premiums and fail to meet the lofty expectations priced into them, their valuations get slammed.

Identifying an attractive investment opportunity is only half the challenge – execution to capitalize on it is also critical.

At GMO, we have a long history of building new strategies to rotate portfolios to the most compelling return sources on offer. Today, nearly half of what Benchmark-Free holds didn’t exist four years ago.

GMO’s Asset Allocation team regularly identifies compelling opportunities and leverages GMO’s infrastructure and other investment teams to build portfolios to capitalize on the specific themes.

We invite you to take a deeper dive into this topic and read the full paper, "A Second Opinion on the 60/40 Default" in its entirety.