Time flies. It has now been over three years since GMO launched our Small Cap Quality Strategy in September 2022. During that period, the world has shifted, and we have navigated unexpected market conditions. We are truly proud to have delivered strong performance relative to the S&P 600, in excess of 4% per annum, net of fees. Our “live” window closely aligns with the modern age of AI, birthed by the release of ChatGPT. This is an era full of promise, but also of disruption. Furthermore, small cap investors have had to tiptoe through minefields such as the banking crisis in 2023 and the “Liberation Day” tariffs in 2025.

Everything looks straightforward in hindsight and a backtest. Lived experience managing a portfolio can prove quite different. Our anniversary and the turn of the calendar year offer a natural point to reflect on the strategy's performance, key drivers of returns, and what we’ve observed along the way. Let us now revisit some of our critical stock picking rules and our observations on how our approach has fared in practice.

Top 10 Insights

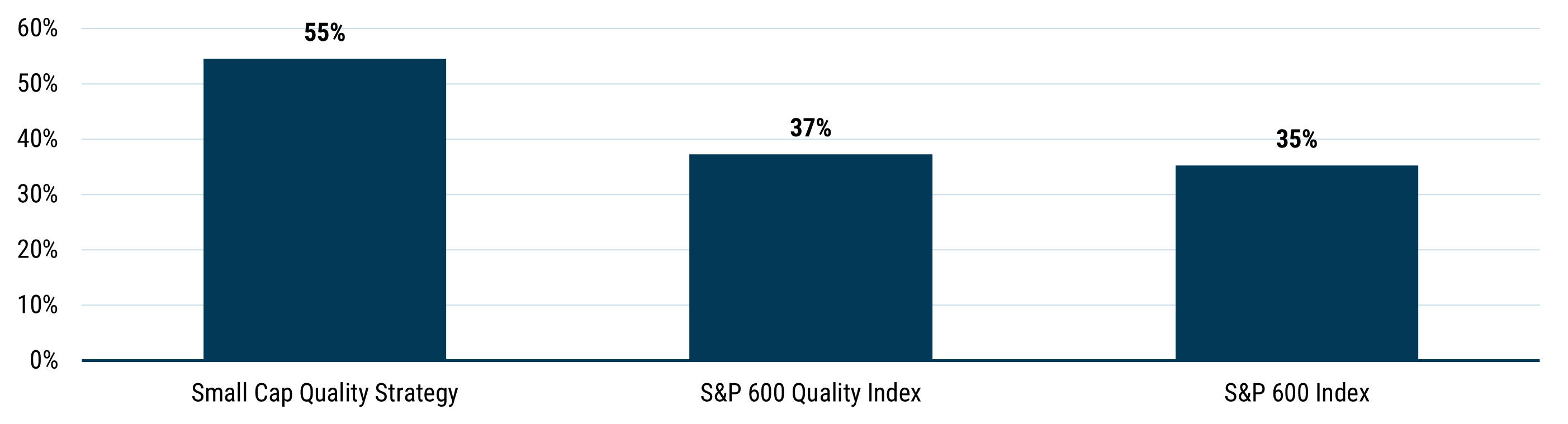

1. Quality Persists in Small Caps

Companies with high and stable profitability, strong balance sheets, and disciplined capital allocation demonstrate a durable advantage that holds across regions and size bands. U.S. Small Caps are no exception, as demonstrated through our systematically defined Small Cap Quality Universe, which serves as the foundation for our stock selection. This universe has a long-term track record of outperforming the S&P 600 and the broader small cap opportunity set. This trend continued over the last 3 years. Small cap quality stocks delivered exceptional outperformance over the period.

While we cannot say with certainty why the quality advantage is so persistent, some behavioral aspects of markets can perhaps help explain it. The market struggles to price the long duration of high returns and outperformance that the best companies can deliver. Valuations implicitly forecast a decay in profitability for even the highest-quality companies, which are, in fact, best positioned to resist reversion to the mean. The compounding that the best companies deliver generates value in the very long term, outside the time horizon of many investors. Career constraints often lead investors to prioritize opportunities with near-term high returns/high risk outcomes, and such distributions are more common in junk stocks than in quality investments.

2. Tracking Error is the Price of Admission

One might expect a behavioral anomaly, such as the outperformance of quality stocks, to be competed away over time by academically oriented investors who discover an attractive opportunity. We are often asked by clients why we believe the quality effect persists, even though it is by now widely known. Variation in returns is a significant part of the story: if you own quality companies, your portfolio will look very different from small-cap benchmarks, which can be challenging for many. The higher tracking error presents a deterrent, preserving the opportunity for those willing to experience a different return profile. Indeed, though small cap quality investing has a very good track record, we have been surprised to find relatively few managers pursuing strategies similar to ours.

3. Weeding Out False Positives is Critical

Factor models and quantitative screens, such as the S&P 600 Quality Index, provide a useful starting point for identifying quality companies. However, our proprietary screening sets a higher bar and is complemented by rigorous fundamental research. This process is essential for identifying and excluding companies that, despite screening as high quality, do not meet our standards for business quality or management. A large part of our value-add lies in weeding out these false positives and constructing a portfolio of truly exceptional businesses.

Exhibit 1: Cumulative Total Shareholder Returns

Data from September 2022-2025

4. Management Quality is Essential

In our view smaller companies tend to be more manageable than larger ones, and C-suite executives generally have a better sense of what is happening at the operating level, as operations are smaller and more comprehensible. That creates more room for a talented manager to create value, or for a weaker manager to destroy value. Direct engagement with company leadership remains a critical component of our research process. We regularly speak with management teams, competitors, and industry experts to gain a nuanced understanding of each company’s prospects and risks. This qualitative insight is particularly critical in the small-cap universe, where management decisions can have a disproportionately large impact. Small cap executives are usually less scripted, so our conversations with them yield more insights.

5. Junk Rallies Burn Bright, but Quality Wins the Race

Living through volatility in real time is different from observing it in a backtest. Periods of outperformance for the lowest-quality companies are always difficult for quality-oriented strategies to stomach. Indeed, we experienced a significant drawdown during such a period starting in July 2024. Patience pays, however, as historically these episodes have ended with sharp reversals and renewed outperformance for quality-focused portfolios. Our risk controls are designed to help mitigate the downside during market stress; however, speculative rallies may temporarily impact our relative performance. That junk rally has been like many others in size and scope over the years, and it will not be the last. Having a clear investment approach enables us to endure these periods of underperformance without losing our nerve or our edge.

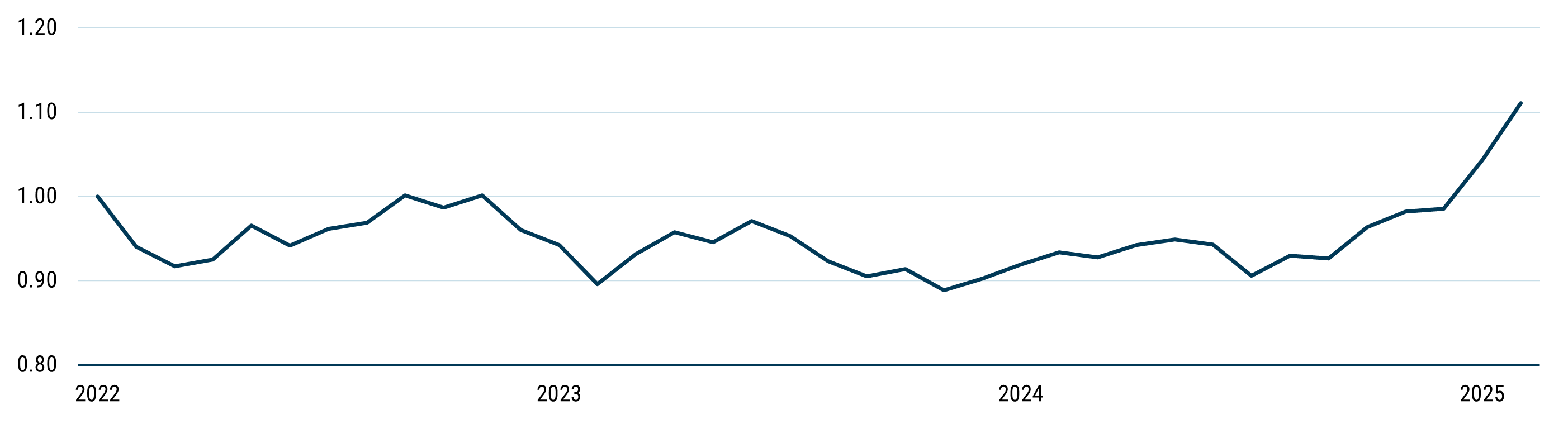

Exhibit 2: Relative Returns of Small Cap Companies with Negative Earnings vs. S&P 600

Source: GMO, Worldscope, S&P

6. Risk Management and Portfolio Construction Matter

Our strategy is built on disciplined portfolio construction and rigorous risk management. We manage the portfolio by maintaining sophisticated quantitative and fundamental analyses of our risks and implicit exposures. In today’s environment, with frequent speculative rallies, we believe thoughtful risk management remains an essential ingredient for long-term outperformance.

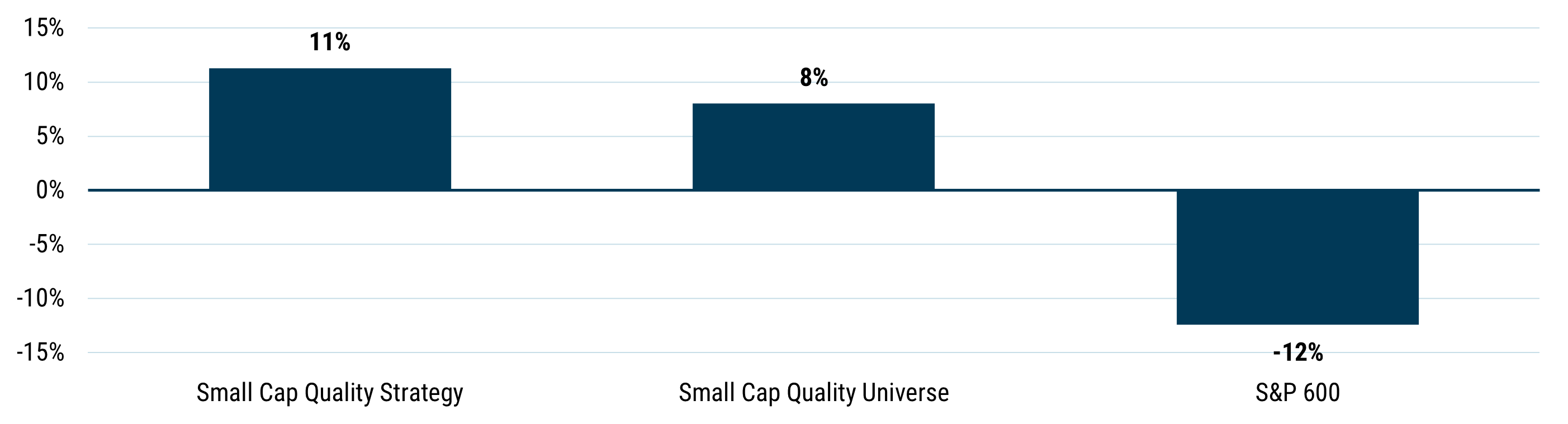

7. The Core of Quality is Earnings Growth

Many small companies remain small because they fail to grow their earnings. Our investment process prioritizes companies with a strong track record of earnings growth, driven by high-returning reinvestments of capital. While short-term valuation swings can impact returns, sustainable long-term outperformance is driven by robust earnings growth. We remain focused on identifying and allocating capital to these companies.

Exhibit 3: Cumulative Earnings Growth

Data from September 2022-2025

8. Private Equity and Acquisition Concerns are Overblown

Clients often ask whether the best small cap companies are being acquired, potentially reducing the opportunity set. Our analysis indicates that acquisitions have declined as a driver of universe exits over time after reaching a peak in the late 1990s. Since the inception of our strategy, only one of our holdings has been acquired, and that was by a strategic buyer rather than a private equity firm. Increased acquisition activity could validate our quality criteria and potentially enhance returns, but it has not been a significant factor in recent years.

Exhibit 4: Acquisitions as a % of Companies in Small Cap Quality Universe

Source: GMO, Worldscope

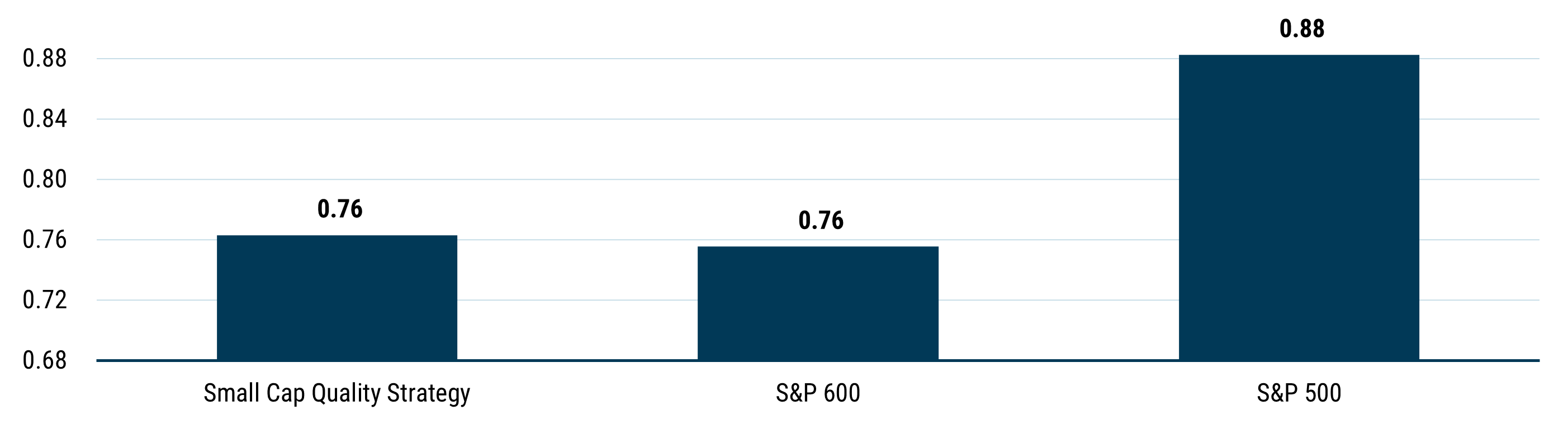

9. AI Beta in Small Caps is Low

By chance, we launched our strategy just before the rollout of ChatGPT 3.5, which catalyzed an explosion of investment in AI; AI has since dominated market narratives and, in many cases, market returns. There are no doubt a few small-cap stocks that do enjoy meaningful exposure to AI-related themes, such as data center buildouts and power generation. Many companies with such exposures have rallied dramatically, quickly graduating from the small cap universe. As a result, small caps have lagged the AI-driven market of the last few years, but as a silver lining, the remaining companies may serve as a diversifier relative to the technology-driven exposures prevalent in large cap indices.

Exhibit 5: Correlation to the iShares A.I. Innovation and Tech Active ETF 1

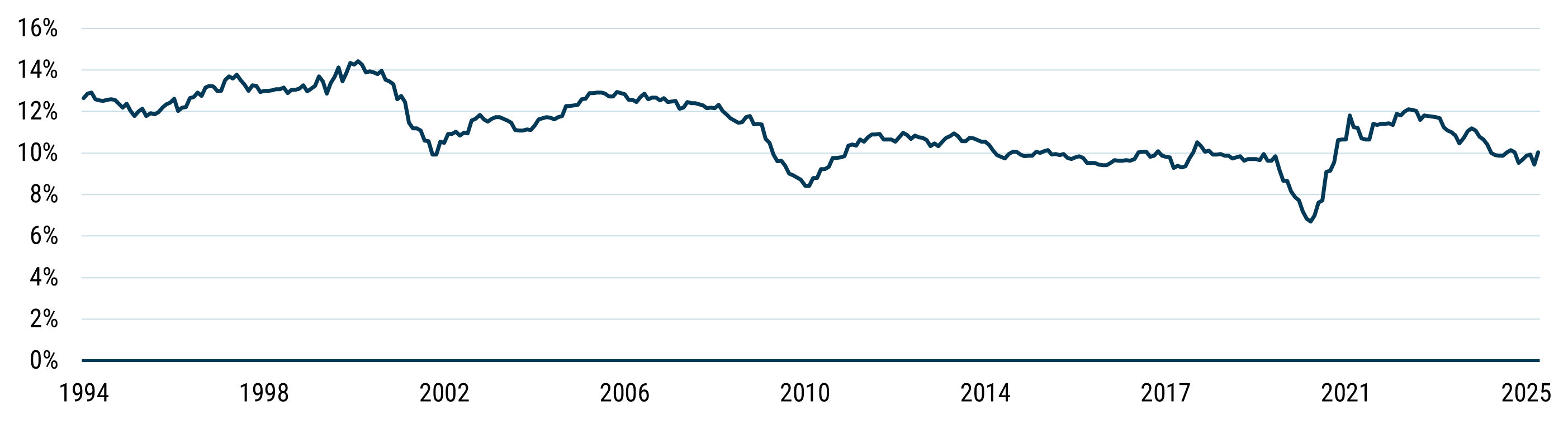

10. A Changing Universe Makes Quality More Valuable Than Ever

The overall quality of small caps stocks has declined relative to that of large caps, with the most significant drop occurring between the mid-1990s and the early 2010s. Some of this decline is cyclical, but structural factors are also at play. As the universe gets “junkier”, a focus on quality will only become more important in delivering attractive small cap returns with a differentiated approach to small cap investing that side-steps the risks of this trend.

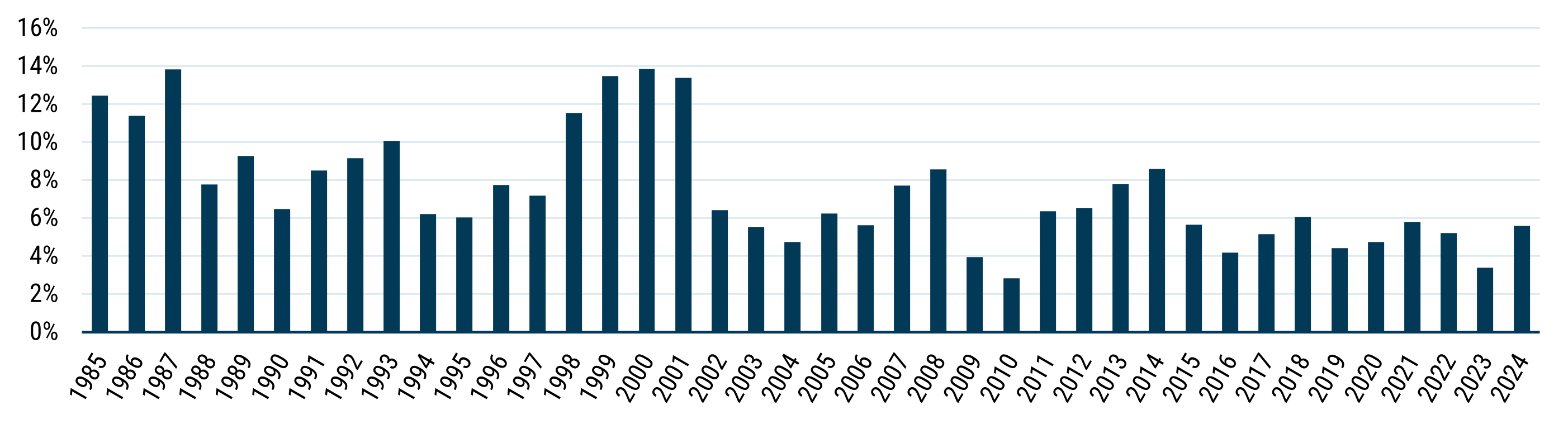

Exhibit 6: Weighted Median ROE of S&P 600

As of Novemeber 2025

The Road Ahead

After three years, our Small Cap Quality Strategy has established a strong track record.

What truly differentiates our approach is a research process that consistently identifies attractive quality opportunities before they become consensus. We go beyond factor definitions: starting with an earnings growth–first discipline, applying a proprietary screen that demands more than generic quality metrics, and validating every idea through hands-on fundamental work and direct dialogue with management teams.

This combination allows us to separate the businesses that genuinely compound from those that only appear attractive on paper. For investors navigating a noisy and uncertain small-cap landscape, we believe our edge (sharper tools, deeper research, and conviction built company by company) positions our strategy to continue delivering durable value creation over time.

iShares A.I. Innovation and Tech Active ETF holdings are predominantly in the US. NVDIA, Broadcom, Alphabet, Taiwan Semiconductor, LAM and Microsoft are about 30% of the ETF.

Disclaimer: The views expressed are the views of Hassan Chowdhry, Tom Hancock, and James Mendelson through April 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be and should not be interpreted as recommendations to purchase or sell such securities.

Copyright © 2026 by GMO LLC. All rights reserved.

iShares A.I. Innovation and Tech Active ETF holdings are predominantly in the US. NVDIA, Broadcom, Alphabet, Taiwan Semiconductor, LAM and Microsoft are about 30% of the ETF.